What Is the Debt Avalanche Method? The Fastest Way to Escape High-Interest Debt

When it comes to paying off debt, there are two popular approaches that dominate personal finance discussions.

The first focuses on psychological momentum through quick wins.

The second focuses on mathematics and minimizing interest costs.

The second strategy is known as the Debt Avalanche Method.

For borrowers carrying high-interest debt, this approach can potentially save thousands of dollars and shorten the path to financial freedom.

In this guide, we’ll explain exactly how the Debt Avalanche Method works, its advantages and disadvantages, and how to determine whether it is the right strategy for your financial situation.

Before starting any debt elimination plan, it is important to build a strong foundation through Money Management and Budgeting.

What Is the Debt Avalanche Method?

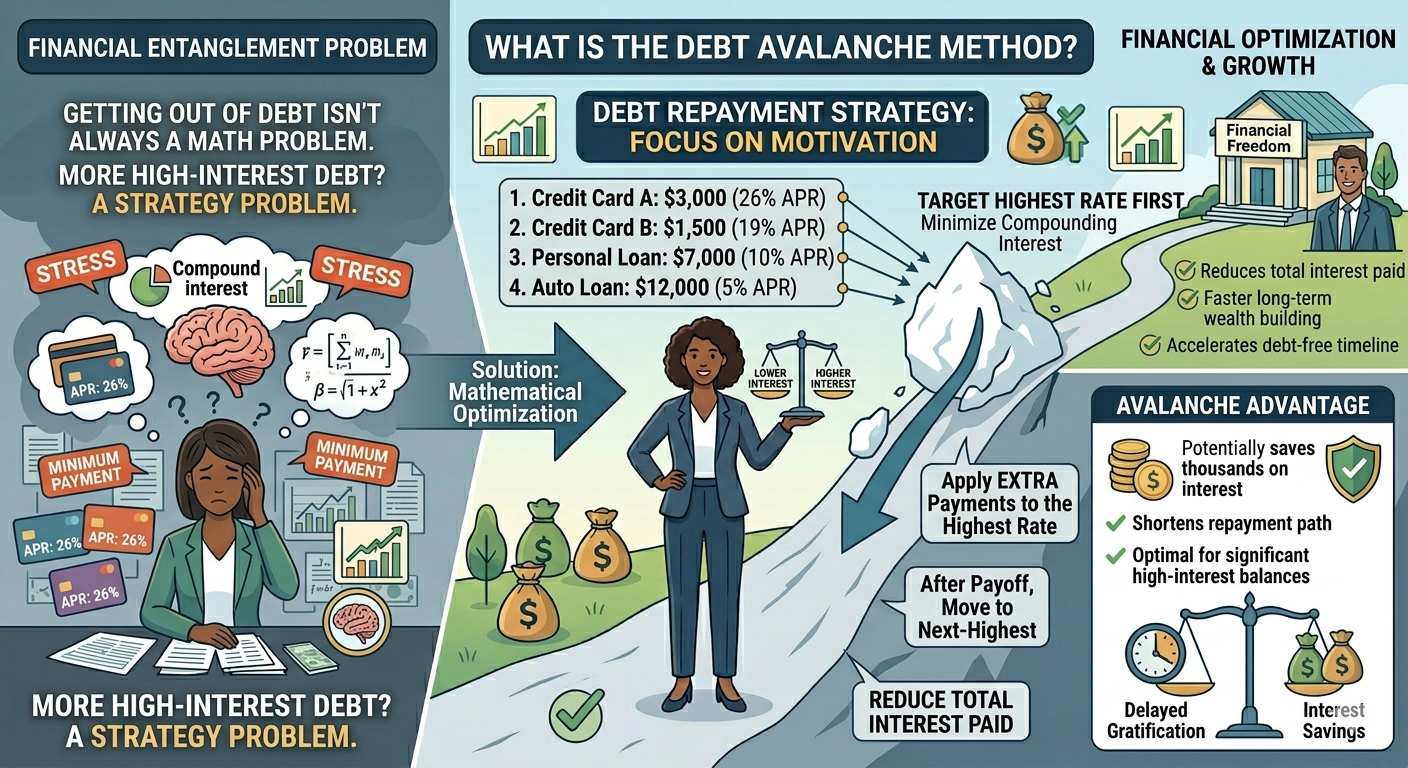

The Debt Avalanche Method is a debt repayment strategy that prioritizes debts with the highest interest rates first.

Instead of focusing on the smallest balance, you focus on the debt that is costing you the most money.

The goal is simple:

Reduce total interest paid and eliminate debt as efficiently as possible.

Under this method, you continue making minimum payments on all debts while directing every extra dollar toward the highest-interest debt.

Once that debt is eliminated, you move to the next-highest interest rate.

This process continues until all debts are paid off.

How the Debt Avalanche Method Works

Imagine you have the following debts:

- Credit Card A: $3,000 balance at 26% APR

- Credit Card B: $1,500 balance at 19% APR

- Personal Loan: $7,000 balance at 10% APR

- Auto Loan: $12,000 balance at 5% APR

Using the Debt Avalanche Method, you would:

- Make minimum payments on all debts.

- Put all extra money toward Credit Card A (26% APR).

- After eliminating Credit Card A, focus on Credit Card B (19% APR).

- Continue working down the list by interest rate.

This approach targets the most expensive debt first and minimizes long-term borrowing costs.

Why the Debt Avalanche Method Is Mathematically Superior

Interest is the hidden enemy of debt repayment.

The longer high-interest debt remains outstanding, the more money it consumes.

The Avalanche Method attacks this problem directly.

By eliminating the highest-interest obligations first, borrowers reduce the amount of interest that compounds over time.

As a result, they often:

- Pay less total interest

- Become debt-free sooner

- Free up cash flow faster

- Build wealth more efficiently

For borrowers focused on maximizing financial efficiency, this method is often considered the optimal strategy.

Debt Avalanche vs. Debt Snowball

The Debt Avalanche Method is frequently compared with the Debt Snowball Method.

Debt Avalanche Method

- Prioritizes highest interest rates first.

- Minimizes total interest costs.

- Often leads to faster long-term financial results.

- Requires patience and discipline.

Debt Snowball Method

- Prioritizes smallest balances first.

- Creates faster psychological wins.

- Builds motivation through early successes.

- May result in higher total interest costs.

If you have already read our guide on the Debt Snowball Method, you know that both strategies can be effective.

The best choice often depends on whether you are more motivated by numbers or by quick victories.

Who Should Use the Debt Avalanche Method?

The Avalanche Method may be ideal if:

- You carry significant high-interest debt.

- You are motivated by financial optimization.

- You can stay disciplined without immediate rewards.

- You want to minimize interest expenses.

- You are focused on long-term financial efficiency.

It is particularly effective for individuals with large credit card balances where interest rates are often extremely high.

The Biggest Challenge: Delayed Gratification

The main weakness of the Avalanche Method is psychological.

Unlike the Snowball Method, early victories may take longer.

A high-interest debt may also have a large balance, meaning it could take months before you completely eliminate your first account.

Some borrowers lose motivation during this phase.

This is why understanding behavioral finance is so important.

As discussed in our article on Investment Psychology, emotions often influence financial outcomes more than mathematics.

How to Maximize Success with the Avalanche Method

1. Create a Detailed Budget

A debt strategy is only effective if it is supported by consistent cash flow management.

Your budget should identify every possible dollar that can be directed toward debt repayment.

2. Eliminate Unnecessary Spending

Reducing discretionary expenses can significantly accelerate your progress.

Reviewing your Spending Habits can help identify opportunities to free up additional cash.

3. Set Meaningful Financial Goals

Debt repayment becomes easier when connected to a larger purpose.

Whether your goal is investing, homeownership, retirement, or financial independence, having a clear destination increases commitment.

Our guide on Financial Goals can help define that vision.

4. Avoid Creating New Debt

The Avalanche Method works best when no new debt is added during the repayment process.

Every new balance slows progress and increases costs.

How the Avalanche Method Supports Financial Freedom

Every dollar saved on interest is a dollar that can be redirected toward building wealth.

Once debt payments disappear, that money can be invested, saved, or used to achieve other financial goals.

This is why debt elimination is often one of the most important milestones on the path toward Financial Freedom.

The sooner you stop paying lenders, the sooner you can start paying yourself.

Final Thoughts

The Debt Avalanche Method is one of the most financially efficient debt repayment strategies available.

By targeting high-interest debt first, it minimizes borrowing costs and accelerates long-term financial progress.

While it may require more patience than the Debt Snowball Method, the potential savings can be substantial.

Ultimately, the best debt strategy is the one you can consistently follow.

If you are disciplined, goal-oriented, and focused on maximizing every dollar, the Debt Avalanche Method may be your fastest route to becoming debt-free.

Because when it comes to debt, every percentage point matters.