Debt Payoff Guide: The First Step Toward Financial Freedom

Debt is one of the biggest obstacles standing between people and financial freedom.

Whether it comes from credit cards, personal loans, student loans, or consumer debt, it can quietly shape your financial life and limit your choices.

But here is the good news:

Debt is not permanent—it is manageable.

With the right strategy, discipline, and structure, you can eliminate debt faster than you think and take control of your financial future.

In this guide, we will break down how debt works, why it becomes overwhelming, and most importantly, how to build a clear path toward becoming debt-free.

If you are building your financial foundation, it is essential to first understand Money Management and Budgeting, because without a clear spending system, debt elimination becomes much harder.

Why Debt Becomes a Problem

Debt itself is not always bad.

Used wisely, it can help you buy a home, invest in education, or grow a business.

The real problem begins when debt becomes uncontrolled or high-interest.

Common reasons people struggle with debt include:

- High-interest credit cards

- Overspending beyond income

- Relying on minimum payments

- Lack of financial planning

- Emergency expenses without savings

Without a clear plan, debt can grow faster than income, creating long-term financial stress. Understanding how credit cards can become a debt trap is an important first step.

Step 1: Understand Your Total Debt Situation

The first step toward solving any financial problem is clarity.

List all your debts, including:

- Total balance

- Interest rate

- Monthly payment

- Remaining term

This simple step often gives people a sense of control they previously lacked.

Step 2: Build a Realistic Budget

A budget is the foundation of every debt payoff strategy.

It helps you understand where your money is going and how much you can realistically allocate toward debt repayment.

If you don’t have a structured budget yet, our guide on Money Management and Budgeting can help you create one step by step. You may also find our step-by-step monthly budgeting guide helpful.

A strong budget ensures that debt repayment becomes a priority, not an afterthought.

Step 3: Choose a Debt Repayment Strategy

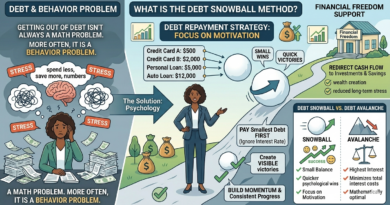

Debt Snowball Method

You pay off the smallest debts first while making minimum payments on others.

This method builds psychological momentum and motivation. Learn exactly how it works in our guide to the Debt Snowball Method.

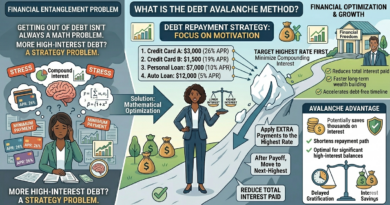

Debt Avalanche Method

You focus on debts with the highest interest rates first.

This method saves more money over time by reducing interest costs. Read our complete guide to the Debt Avalanche Method.

Debt Consolidation

Multiple debts are combined into a single loan with a potentially lower interest rate.

This simplifies payments and can reduce monthly financial pressure. Learn when debt consolidation with a personal loan makes sense.

Step 4: Stop Creating New Debt

One of the most important steps is preventing new debt accumulation.

This requires behavior change, not just financial planning.

Key strategies include:

- Avoid unnecessary credit card usage

- Use cash or debit for daily expenses

- Delay non-essential purchases

- Track spending consistently

Understanding your spending behavior is crucial here. You can explore this further in our article on Spending Habits. If impulse purchases are your biggest challenge, our guide on how to stop impulse spending can help.

Step 5: Build an Emergency Fund

One of the main reasons people fall back into debt is unexpected expenses.

An emergency fund acts as a financial buffer.

Even a small fund covering one to three months of expenses can prevent new debt from forming during financial shocks.

This is why saving is such a critical part of financial stability. You can learn more in our guide on The Ultimate Saving Guide.

Psychological Side of Debt

Debt is not just a financial issue—it is also an emotional one.

Many people feel stress, anxiety, or even shame because of debt.

This emotional burden often leads to avoidance, which makes the situation worse.

The key is to replace avoidance with structure.

Once you have a plan, debt becomes a mathematical problem—not an emotional one. Building the right financial mindset can make staying committed to your repayment plan much easier.

Common Mistakes in Debt Repayment

Only Paying Minimum Amounts

This extends repayment time and increases total interest significantly. Learn why in our article about the minimum payment trap.

Ignoring High-Interest Debt

Not prioritizing expensive debt leads to unnecessary financial loss.

Lack of Budget Discipline

Without consistent budgeting, debt-free progress is often temporary.

How Debt Freedom Builds Financial Freedom

Eliminating debt is not just about reducing liabilities.

It is about unlocking financial potential.

Once debt is removed, money that was previously used for payments can be redirected toward:

- Savings

- Investments

- Retirement accounts

- Wealth-building opportunities

This shift creates long-term financial momentum and moves you closer to financial freedom.

Final Thoughts

Debt does not define your financial future.

Your decisions do.

With a clear plan, disciplined budgeting, and consistent action, debt can be eliminated systematically.

The journey to financial freedom often begins with one simple step: deciding to take control.

Once you do that, every payment becomes a step closer to financial independence.