How to Improve Your Credit Score Fast: Proven Strategies That Actually Work

If you’re planning to apply for a mortgage, auto loan, personal loan, or new credit card, you’ve probably wondered:

“What’s the fastest way to improve my credit score?”

It’s an important question—but it often leads people toward unrealistic promises.

The truth is that there is no legitimate overnight fix for your credit score.

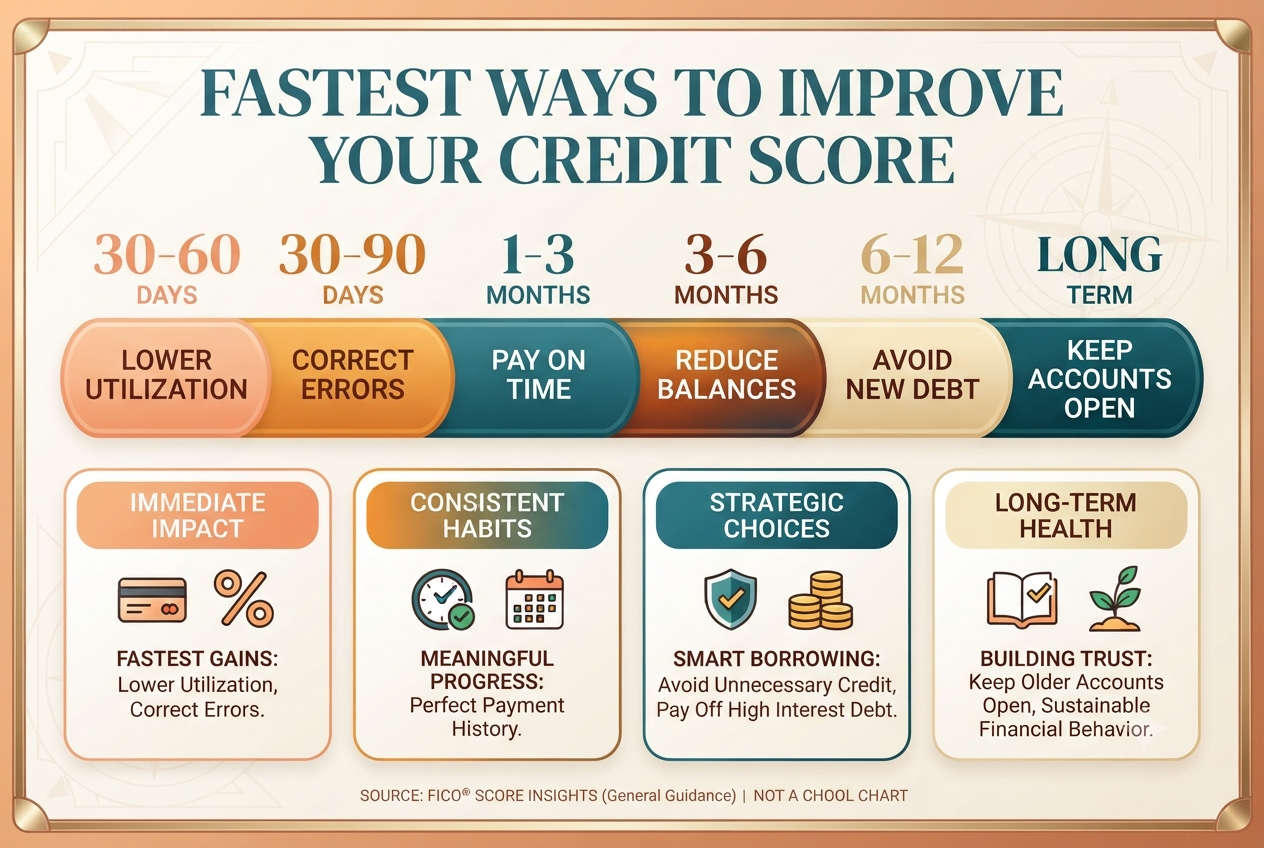

However, some actions can produce noticeable improvements within 30 to 90 days, while others build stronger credit over the long term. The fastest gains typically come from lowering credit card balances, correcting reporting errors, and maintaining perfect payment history.

This guide explains which strategies have the biggest impact, which mistakes slow your progress, and how to improve your FICO Score as quickly—and responsibly—as possible.

Before focusing on your credit score, make sure your finances are built on a solid foundation with Money Management and Budgeting. Strong financial habits always come before strong credit.

Can You Improve Your Credit Score Quickly?

Yes—but only if the factors hurting your score are ones you can change immediately.

For many borrowers, the quickest improvements come from:

- Paying down high credit card balances.

- Reducing credit utilization.

- Correcting inaccurate information on credit reports.

- Bringing overdue accounts current.

More serious issues—such as collections, loan defaults, or bankruptcies—typically require much more time to recover from.

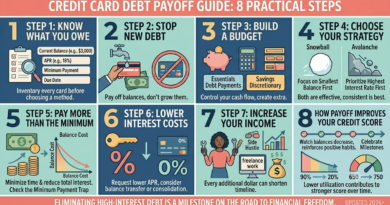

Strategy #1: Lower Your Credit Utilization

This is often the fastest way to increase a credit score.

Credit utilization measures how much of your available revolving credit you’re currently using.

For example:

- Credit limit: $10,000

- Balance: $6,000

- Utilization: 60%

Paying that balance down to $2,000 lowers utilization to 20%, which many scoring models view much more favorably. Experts generally recommend staying below 30%, while keeping utilization under 10% may provide additional benefits.

For more guidance, read our article on Choosing the Right Credit Card Limit.

Strategy #2: Never Miss a Payment

Your payment history is the single most influential component of a FICO Score.

Even one late payment can significantly reduce your score and remain on your credit report for years.

Setting up automatic payments or payment reminders can help ensure every bill is paid on time.

Strategy #3: Review Your Credit Reports

Credit reports occasionally contain errors.

You may find:

- Incorrect late payments.

- Accounts that don’t belong to you.

- Duplicate balances.

- Outdated information.

Disputing inaccurate information with the credit bureaus can sometimes produce one of the fastest legitimate score improvements.

Strategy #4: Avoid Applying for Unnecessary Credit

Every hard credit inquiry can have a small temporary impact on your score.

Submitting several credit applications within a short period may also signal higher borrowing risk to lenders.

Only apply for new credit when it genuinely supports your financial goals.

Strategy #5: Keep Older Accounts Open

The length of your credit history matters.

Closing your oldest credit card may shorten your average account age and reduce your available credit, potentially increasing your utilization ratio.

If an older account has no annual fee and fits your financial plan, keeping it open may benefit your long-term credit profile.

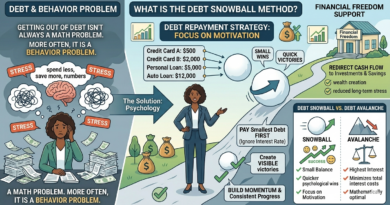

Strategy #6: Pay Off High-Interest Debt

Reducing debt improves more than your credit score.

It also:

- Lowers interest costs.

- Improves cash flow.

- Reduces financial stress.

- Creates room for future savings and investing.

If you’re carrying multiple balances, these guides can help:

Common Mistakes That Slow Credit Score Growth

Avoid these common errors:

- Maxing out credit cards.

- Making only minimum payments.

- Opening multiple new accounts at once.

- Ignoring reporting mistakes.

- Believing companies that promise instant credit repair.

Legitimate negative information generally cannot be legally removed simply because you pay someone to “repair” your credit. Sustainable improvement comes from responsible financial behavior.

How Quickly Can Your Score Increase?

The timeline depends on what’s lowering your score.

- 30–60 days: Lower utilization and corrected reporting errors may produce noticeable improvements.

- 3–6 months: Consistent on-time payments and lower balances often lead to meaningful progress.

- 6–12 months or longer: Recovering from missed payments or significant financial setbacks requires patience.

Our detailed guide on How Long It Takes to Improve Your Credit Score explains these timelines in greater depth.

Why Improving Your Credit Score Matters

A stronger credit profile can help you:

- Qualify for lower APRs.

- Access better credit card offers.

- Receive more competitive mortgage rates.

- Reduce borrowing costs.

- Increase overall financial flexibility.

Even a modest improvement can translate into substantial savings over the life of a mortgage or personal loan.

Focus on Long-Term Financial Health

The fastest improvements come from smart decisions.

The biggest improvements come from repeating those decisions month after month.

Responsible borrowing, disciplined budgeting, and consistent repayment habits not only improve your credit score—they strengthen your overall financial future.

Our guide on Financial Freedom explores how strong credit supports long-term wealth building.

Final Thoughts

If you’re looking for the fastest way to improve your credit score, start with the actions that have the greatest impact:

- Pay every bill on time.

- Reduce your credit card balances.

- Keep your credit utilization low.

- Review your credit reports regularly.

- Avoid unnecessary new debt.

There are no shortcuts to excellent credit.

But with consistent financial habits, patience, and a clear strategy, your credit score can steadily improve—and so can every financial opportunity that comes with it.