How to Pay Off Credit Card Debt: A Step-by-Step Guide to Financial Freedom

Credit cards can be incredibly useful financial tools.

They offer convenience, fraud protection, rewards, and can even help build a strong credit history.

But when balances continue to grow and interest starts compounding, credit cards can quickly become one of the most expensive forms of consumer debt.

The good news?

Credit card debt is not permanent.

With a clear plan and consistent action, you can eliminate it and redirect your income toward building wealth instead of paying interest.

This guide walks you through a practical, step-by-step strategy to pay off credit card debt while improving your long-term financial health.

Before starting your debt payoff journey, make sure you have a solid understanding of Money Management and Budgeting, because every successful debt repayment plan begins with controlling your cash flow.

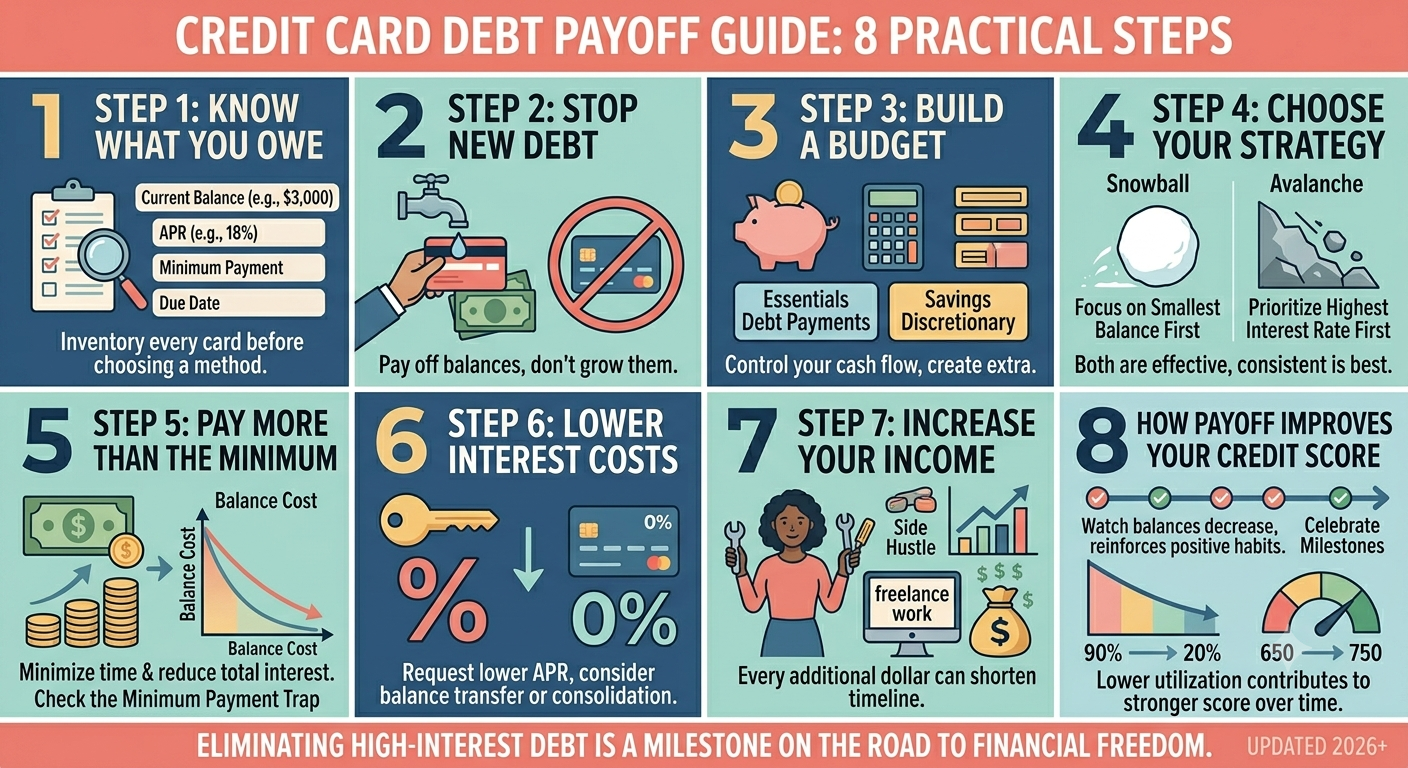

Step 1: Know Exactly What You Owe

You cannot solve a financial problem you haven’t clearly defined.

Create a list of every credit card you have and include:

- Current balance

- Annual Percentage Rate (APR)

- Minimum monthly payment

- Payment due date

- Available credit

Seeing the complete picture allows you to build a realistic payoff strategy instead of making decisions based on guesswork. Financial educators consistently recommend starting with a full inventory of your balances before choosing a repayment method.

Step 2: Stop Creating New Debt

Paying off existing balances while continuing to use your credit cards is like trying to empty a bathtub with the faucet still running.

Until your balances are under control:

- Avoid unnecessary purchases.

- Use cash or your debit card for everyday spending whenever possible.

- Remove saved card information from shopping apps if impulse spending is a challenge.

Your first priority is stopping the debt from growing.

Step 3: Build a Realistic Monthly Budget

Debt repayment requires free cash flow.

Review your monthly income and categorize your expenses into:

- Essential living expenses

- Debt payments

- Savings

- Discretionary spending

Even relatively small reductions in discretionary spending can significantly accelerate debt repayment over time.

If you haven’t created one yet, follow our guide on How to Create a Realistic Monthly Budget.

Step 4: Choose Your Debt Payoff Strategy

Once you know how much extra money you can dedicate each month, choose a repayment strategy.

Debt Snowball Method

Focus on paying off your smallest balance first while making minimum payments on all other cards.

This method creates quick psychological wins and helps maintain motivation.

Learn more in our guide to the Debt Snowball Method.

Debt Avalanche Method

Prioritize the card with the highest interest rate while continuing minimum payments on the others.

This approach minimizes total interest costs and is mathematically the most efficient strategy.

Read more in our guide to the Debt Avalanche Method.

Both strategies are effective—the best one is the one you can consistently follow.

Step 5: Pay More Than the Minimum

Making only the minimum payment keeps your account in good standing, but it often keeps you in debt for years.

Most of each payment goes toward interest instead of reducing the principal balance.

Even an extra $50 or $100 each month can dramatically shorten your repayment timeline and reduce total interest paid.

Our article on the Minimum Payment Trap explains why relying on minimum payments is so costly.

Step 6: Lower Your Interest Costs

Reducing your interest rate can help more of each payment go toward your balance.

Depending on your situation, you may be able to:

- Request a lower APR from your card issuer.

- Transfer your balance to a promotional low- or 0% APR card if you qualify.

- Consider a debt consolidation loan if it meaningfully reduces your borrowing costs.

These options aren’t right for everyone, but they can significantly accelerate repayment when used responsibly.

Step 7: Increase Your Income

While reducing expenses helps, increasing income can often have an even greater impact.

Consider:

- Freelance work

- Consulting

- Gig economy opportunities

- Part-time employment

- Selling unused items

Every additional dollar can shorten your debt payoff timeline.

Step 8: Track Your Progress

Debt repayment is a long-term process.

Celebrate milestones along the way.

Watching balances decrease provides motivation and reinforces positive financial habits.

Progress—not perfection—is what creates lasting financial change.

How Paying Off Credit Card Debt Improves Your Credit Score

Reducing balances can improve your credit profile by lowering your credit utilization ratio.

Lower utilization is generally viewed favorably by lenders and may contribute to a stronger credit score over time.

To learn more, read our guide on Credit Scores and Financial Reputation.

How to Stay Out of Credit Card Debt

Becoming debt-free is only part of the journey.

Staying debt-free requires lasting financial habits.

Successful credit card users typically:

- Pay their statement balance in full.

- Keep credit utilization low.

- Use credit cards only for planned purchases.

- Maintain an emergency fund.

- Track spending consistently.

For more long-term strategies, read our guide on the Smartest Credit Card Strategy.

Credit Card Debt and Financial Freedom

Every dollar spent on interest is a dollar that cannot be invested, saved, or used to build wealth.

Paying off your credit cards frees future income for opportunities that create long-term financial security.

This is why eliminating high-interest debt is one of the most important milestones on the road to Financial Freedom.

Final Thoughts

Credit card debt may feel overwhelming today, but it is a solvable problem.

Start by understanding your balances, creating a realistic budget, choosing a repayment strategy, and consistently paying more than the minimum.

Small actions repeated every month create extraordinary results over time.

The goal isn’t simply to eliminate debt.

It’s to build a financial life where your money works for you instead of your lenders.