How Long Does It Take to Improve Your Credit Score? A Realistic Timeline for Building Better Credit

One of the most common questions people ask after deciding to improve their finances is:

“How long will it take for my credit score to go up?”

It’s a fair question—but there isn’t a single answer.

Some improvements can appear within a month or two, while rebuilding credit after serious financial setbacks may take several years.

The important thing to understand is this:

Credit scores reward consistent financial behavior—not quick fixes.

If you’re patient and follow good financial habits, your credit score will usually improve over time. The timeline depends on what is affecting your score and how consistently you manage your credit.

In this guide, we’ll explain what influences your credit score, how long different improvements typically take, and the most effective ways to accelerate your progress.

Before focusing on your credit score, it’s important to build a strong financial foundation with Money Management and Budgeting. Healthy credit starts with healthy financial habits.

Why Credit Scores Don’t Change Overnight

Your credit score is based on information reported by lenders to the major credit bureaus.

Most lenders update account information about once every billing cycle—not every day.

That means even if you pay off a large balance today, it may take several weeks before the change appears in your credit report and affects your score.

Credit improvement is a process of building trust over time.

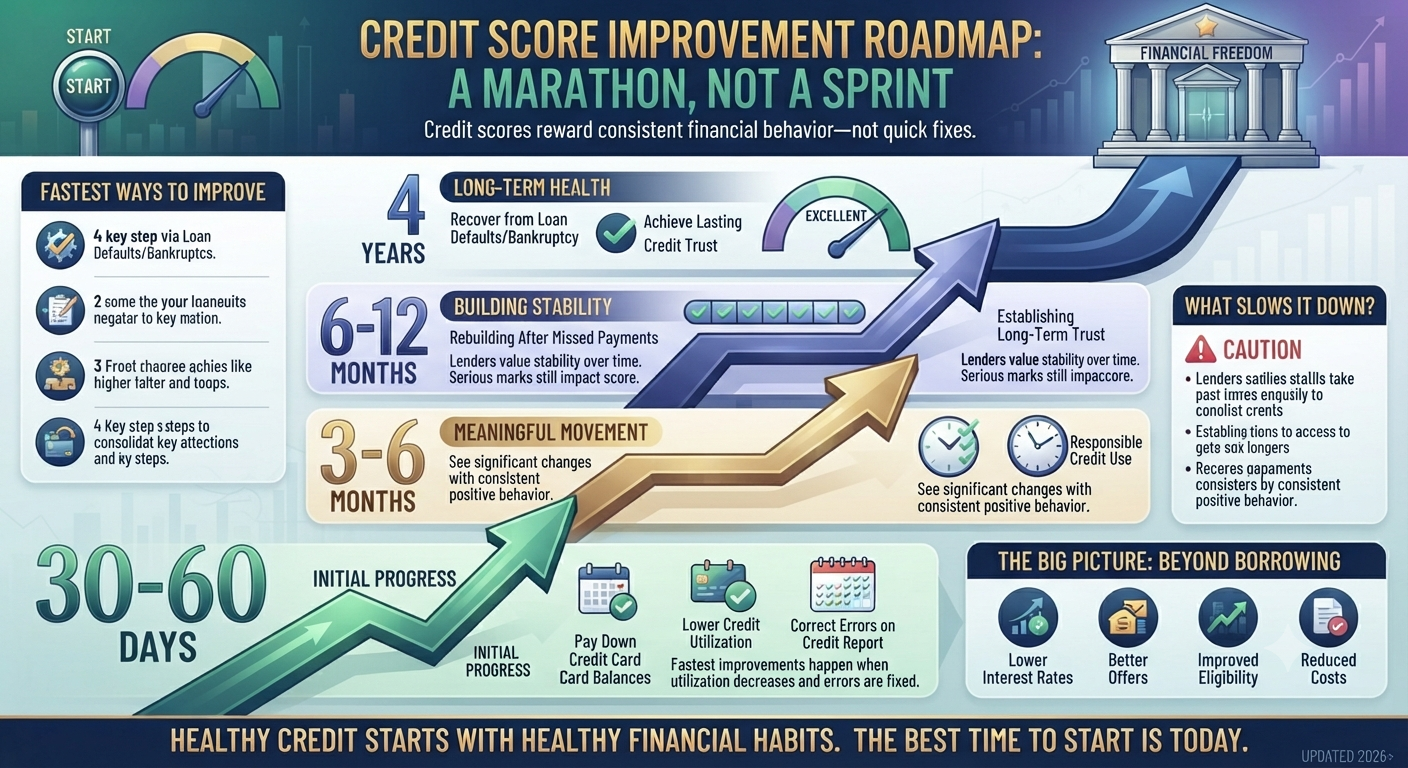

A Realistic Credit Score Improvement Timeline

30 to 60 Days

Some of the fastest improvements happen when you:

- Pay down high credit card balances.

- Lower your credit utilization ratio.

- Correct errors on your credit report.

- Catch up on recently overdue accounts.

Because utilization updates monthly, many people begin seeing positive movement within one or two billing cycles.

3 to 6 Months

With consistent on-time payments and responsible credit use, many borrowers see meaningful improvements within several months.

This is especially true if the original score decline resulted from high credit card balances rather than severe delinquencies.

6 to 12 Months

If you’ve experienced missed payments or significant financial challenges, rebuilding your credit often requires six months or longer of consistent positive behavior.

Lenders value stability over time.

Several Years

Serious negative events—such as loan defaults, collections, or bankruptcy—take much longer to recover from.

Although their impact gradually decreases, these negative marks can remain on your credit report for several years.

The Fastest Ways to Improve Your Credit Score

1. Pay Every Bill on Time

Your payment history is the single most important factor in most credit scoring models.

Even one missed payment can significantly reduce your score.

Setting up automatic payments can help you avoid accidental late payments.

2. Reduce Credit Card Balances

High credit utilization is one of the quickest factors you can improve.

Many financial experts recommend keeping utilization below 30%, while even lower levels may provide additional benefits.

Our guide on Choosing the Right Credit Card Limit explains why utilization matters so much.

3. Avoid Applying for Too Much New Credit

Each hard credit inquiry can have a small temporary impact on your score.

Submitting multiple applications within a short period may signal increased borrowing risk.

Only apply for new credit when you genuinely need it.

4. Check Your Credit Report for Errors

Incorrect late payments, duplicate accounts, or reporting mistakes can lower your score unnecessarily.

Review your credit reports regularly and dispute any inaccuracies you find.

What Slows Down Credit Score Recovery?

Several behaviors can delay your progress:

- Missing payments.

- Maxing out credit cards.

- Frequently opening new accounts.

- Ignoring existing debt.

- Closing long-established credit accounts without a good reason.

Improving your credit score isn’t just about doing the right things—it’s also about avoiding the wrong ones.

Credit Scores and Debt Management Go Hand in Hand

If you’re carrying significant high-interest debt, improving your credit score often begins with reducing what you owe.

Depending on your situation, strategies like the Debt Snowball Method, the Debt Avalanche Method, or Debt Consolidation may help accelerate both debt repayment and long-term credit improvement.

Can You Improve Your Credit Score Quickly?

Sometimes.

If your score is being held back primarily by high credit utilization or reporting errors, noticeable improvements may happen within one or two months.

However, if your report contains late payments, defaults, or collections, meaningful improvement usually requires patience and consistent financial behavior.

There are no legitimate shortcuts.

Every lasting improvement is built on responsible borrowing and timely repayment.

Credit Improvement Is About More Than Borrowing

A higher credit score isn’t just about qualifying for loans.

It can also help you:

- Qualify for lower interest rates.

- Access better credit card offers.

- Improve mortgage eligibility.

- Reduce borrowing costs over time.

- Increase overall financial flexibility.

That’s why improving your credit should be viewed as part of your broader financial plan—not as an isolated goal.

Our guide on Financial Freedom explains how strong credit supports long-term wealth building.

Final Thoughts

Improving your credit score isn’t a sprint—it’s a marathon.

Some progress can happen within weeks.

Major improvements often take months.

Recovering from serious financial setbacks may take years.

But every on-time payment, every dollar of debt reduced, and every responsible financial decision moves you in the right direction.

The best time to start improving your credit score was yesterday.

The second-best time is today.