What Happens If Your Credit Score Drops? The Hidden Costs of Bad Credit

Many people don’t think about their credit score until they apply for a loan.

Then reality sets in.

A lower credit score doesn’t simply reduce your chances of getting approved.

It can quietly increase the cost of borrowing, limit financial opportunities, and even affect parts of your life that have nothing to do with loans.

In other words, a declining credit score creates hidden costs that many people never see coming.

Understanding these consequences can help you protect both your financial health and your future opportunities.

Before focusing on your credit score, it’s important to build strong financial habits with Money Management and Budgeting. Good credit is usually the result of consistent financial discipline.

What Does a Lower Credit Score Mean?

Your FICO Score is designed to estimate how likely you are to repay borrowed money on time.

When your score falls, lenders generally view you as a higher-risk borrower.

That doesn’t always mean you’ll be denied credit.

It often means you’ll pay more to borrow the same amount of money. Scores below 580 are generally considered “Poor” under the FICO scoring model, making access to affordable credit much more difficult.

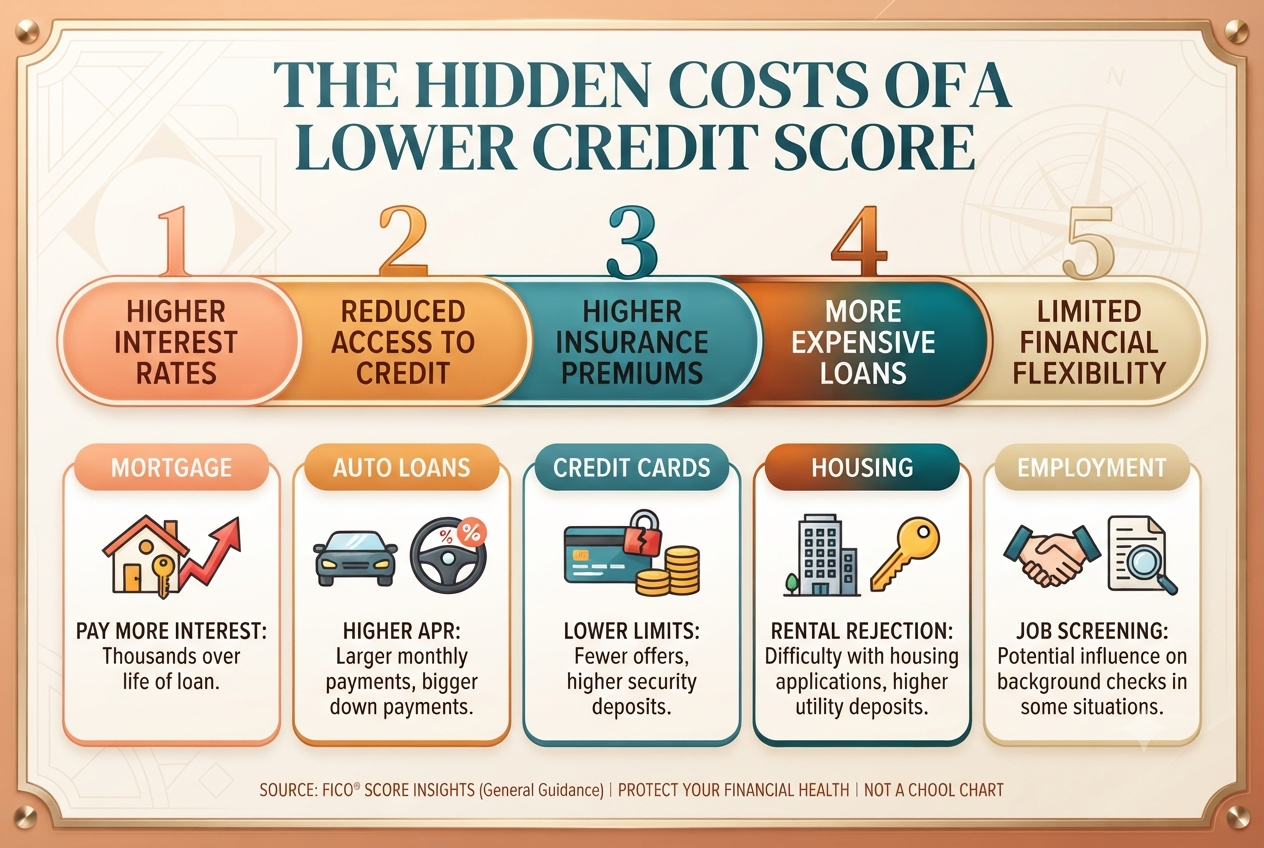

Higher Interest Rates

This is usually the first—and most expensive—consequence.

Even if you’re approved for financing, a lower credit score often results in a higher Annual Percentage Rate (APR).

That means:

- Higher monthly payments.

- More interest over the life of the loan.

- Greater overall borrowing costs.

For example, borrowers with stronger credit profiles often qualify for significantly lower mortgage rates than those with weaker scores, potentially saving tens of thousands of dollars over the life of a home loan.

Reduced Access to Credit

Some lenders may decline your application altogether.

Others may approve a much smaller loan than you requested.

You could also receive:

- Lower credit card limits.

- Fewer promotional financing offers.

- Higher security deposit requirements.

A low credit score limits financial flexibility at the very time you may need it most.

Higher Costs Beyond Loans

Many people are surprised to learn that credit scores can influence more than lending decisions.

Depending on where you live and applicable regulations, your credit history may also affect:

- Auto insurance premiums.

- Rental housing applications.

- Utility deposits.

- Certain employment background screenings.

Not every employer or insurer uses credit information, and rules vary by state and country, but poor credit can increase costs or reduce available options in some situations.

Buying a Home Becomes More Expensive

Mortgage lenders carefully evaluate credit scores.

Even a relatively small drop can lead to a noticeably higher mortgage rate.

Over a 30-year mortgage, that difference may translate into thousands—or even tens of thousands—of dollars in additional interest payments.

If homeownership is one of your long-term goals, protecting your credit score should be part of your financial strategy.

Auto Loans Become More Expensive

The same principle applies to vehicle financing.

Borrowers with lower credit scores often receive:

- Higher interest rates.

- Larger required down payments.

- Shorter financing options.

That means paying more every month for the same vehicle.

Your Financial Flexibility Shrinks

A healthy credit score provides options.

You can refinance.

You can qualify for better credit cards.

You can respond more easily to unexpected financial needs.

When your score drops, those options become more limited.

Financial flexibility is one of the most valuable assets you can have—and your credit score plays a major role in preserving it.

What Causes Credit Scores to Fall?

Several common financial habits can lower your score:

- Missing payments.

- Maxing out credit cards.

- Applying for multiple new credit accounts in a short period.

- Accounts entering collections.

- Loan defaults.

High credit utilization and late payments are among the most common reasons scores decline.

Can a Lower Credit Score Be Repaired?

Absolutely.

Most credit score declines are not permanent.

With consistent financial habits, many borrowers gradually rebuild their credit.

Focus on:

- Making every payment on time.

- Reducing credit card balances.

- Keeping credit utilization low.

- Avoiding unnecessary new credit applications.

- Reviewing your credit reports for errors.

Our guide on How to Improve Your Credit Score Fast explains these strategies in detail.

How Debt Affects Your Credit Score

Large credit card balances and unmanaged debt often contribute to lower credit scores.

If debt has become difficult to manage, these guides can help:

Protecting Your Credit Is Protecting Your Wealth

Your credit score is more than a number.

It influences how much you’ll pay to borrow, the financial products available to you, and how easily you can reach major life goals.

Protecting your credit today can reduce costs for years to come.

Our article on What Is a Good Credit Score? explains which score ranges are ideal for different financial objectives.

Final Thoughts

A lower credit score doesn’t just make borrowing harder.

It can quietly increase the cost of many financial decisions throughout your life.

The good news is that credit scores are dynamic.

Every on-time payment, every reduction in debt, and every responsible financial decision helps strengthen your financial profile.

Think of your credit score as a long-term financial asset.

The better you protect it today, the more opportunities—and lower costs—you’ll enjoy tomorrow.