Credit Cards: Financial Freedom Tool or a Debt Trap?

Credit cards are one of the most widely used financial tools in the modern world.

Used correctly, they can provide convenience, rewards, and even help build a strong credit history.

Used incorrectly, they can quickly turn into one of the most expensive forms of debt.

This raises an important question:

Are credit cards a path to financial freedom or a trap that keeps people in debt?

The answer depends entirely on how you use them.

In this article, we will break down how credit cards work, their advantages and risks, and how to use them responsibly to support your financial goals.

If you are building your financial foundation, it is helpful to first understand Money Management and Budgeting and how spending behavior impacts your financial health.

How Credit Cards Work

A credit card allows you to borrow money from a bank or financial institution up to a certain limit.

You can use this borrowed money to make purchases and repay it later.

If you pay your balance in full each month, you typically avoid interest charges.

If you carry a balance, interest is applied—often at very high rates compared to other forms of borrowing.

Understanding how interest is calculated can help you better understand the true cost of carrying credit card debt.

The Advantages of Credit Cards

1. Convenience and Flexibility

Credit cards make it easy to make purchases both online and in-store without carrying cash.

2. Building Credit History

Responsible credit card usage helps build a strong credit score, which is important for loans, mortgages, and financial credibility in many countries, especially the United States.

3. Rewards and Cashback

Many credit cards offer rewards such as cashback, travel points, or discounts on purchases.

4. Fraud Protection

Credit cards often provide stronger fraud protection compared to debit cards or cash.

5. Emergency Financial Buffer

They can serve as a short-term financial safety net in emergencies when cash is not immediately available.

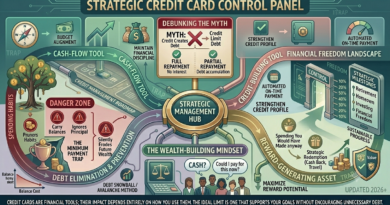

The Risks of Credit Cards

1. High Interest Rates

One of the biggest risks is carrying a balance.

Interest charges can quickly accumulate and turn small purchases into long-term debt.

2. Overspending Behavior

Because credit cards feel like “future money,” people tend to spend more than they can afford. Developing healthier spending habits is essential for avoiding this trap.

3. Minimum Payment Trap

Paying only the minimum amount keeps you in debt longer and increases total interest paid. Learn more in our guide on the minimum payment trap.

4. Psychological Detachment from Money

Digital payments reduce the feeling of spending real money, which can lead to poor financial decisions. Understanding your financial psychology can help you recognize these behaviors.

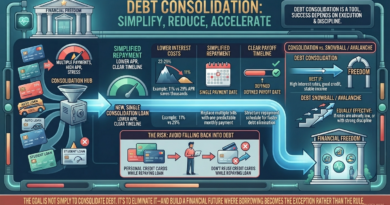

Credit Cards and Debt Cycles

One of the most dangerous financial patterns is the credit card debt cycle.

It usually starts with small balances that are not paid in full.

Over time, interest accumulates, and the minimum payment becomes harder to manage.

This creates a cycle where debt grows faster than repayment.

Breaking this cycle requires discipline, awareness, and a structured financial plan. If you’re already carrying high-interest balances, our Credit Card Debt Payoff Guide can help you create an effective repayment strategy.

This is why strong financial foundations such as Financial Goals are essential for long-term stability.

How to Use Credit Cards Responsibly

1. Pay Your Balance in Full Every Month

The most important rule is simple: never carry a balance if you can avoid it.

2. Use Credit Cards for Planned Expenses Only

Avoid using credit cards for impulse purchases or unplanned spending. Following these strategies to stop impulse spending can make this much easier.

3. Set a Spending Limit Below Your Credit Limit

Just because you can spend more does not mean you should. You may also benefit from understanding how much credit card limit you should have.

4. Track Every Purchase

Include credit card spending in your monthly budget.

If you need help with this, our guide on Money Management and Budgeting can help you build a structured system.

5. Avoid Multiple Unnecessary Cards

Too many credit cards can make it harder to track spending and increase financial risk.

Credit Cards in a Healthy Financial System

Credit cards are neither good nor bad on their own.

They are tools.

And like any tool, their impact depends on how they are used.

In a healthy financial system, credit cards are used strategically:

- Expenses are planned

- Balances are paid in full

- Spending is tracked

- Credit is managed responsibly

When combined with strong budgeting habits and clear financial goals, credit cards can support—not harm—your financial journey. You can also explore the smartest credit card strategy to maximize benefits while minimizing risk.

Final Thoughts

Credit cards can either accelerate your financial progress or slow it down significantly.

The difference lies in behavior, discipline, and awareness.

If you treat credit cards as a convenience tool rather than extra income, they can become part of a healthy financial system.

But if you lose control of spending, they can quickly turn into a debt trap that is difficult to escape.

Financial success is not about avoiding tools—it is about using them wisely.