What Is a Good Credit Score? The Ideal FICO Score for Every Financial Goal

Many people ask the same question:

“What credit score do I actually need?”

The answer depends on what you’re trying to accomplish.

You don’t need a perfect 850 FICO Score to qualify for most financial products.

In fact, many borrowers can secure competitive loan offers with a score that is well below the maximum.

The key is understanding which credit score range aligns with your financial goals.

Whether you’re applying for a credit card, financing a car, buying a home, or simply trying to reduce borrowing costs, knowing your target score helps you focus on meaningful progress instead of chasing perfection.

In this guide, we’ll explain the major FICO Score ranges, what lenders typically expect, and which score you should aim for depending on your financial objectives.

Before working on your credit score, make sure your overall finances are built on a strong foundation with Money Management and Budgeting. Healthy credit starts with healthy financial habits.

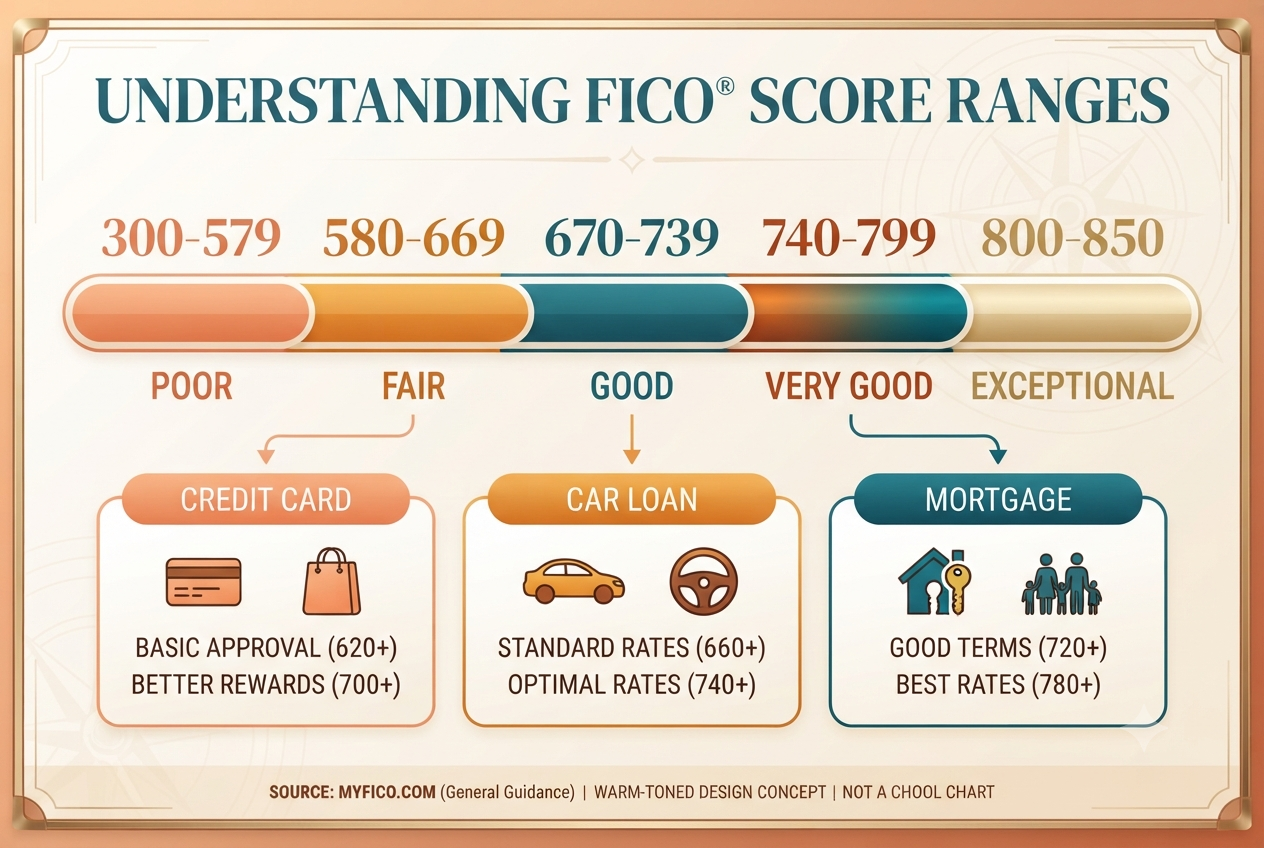

Understanding the FICO Score Range

The most widely used credit scoring model in the United States is the FICO Score, which ranges from 300 to 850. Most major lenders rely on some version of a FICO Score when evaluating loan applications.

- 300–579: Poor

- 580–669: Fair

- 670–739: Good

- 740–799: Very Good

- 800–850: Exceptional

While higher scores generally qualify for better interest rates and loan terms, there is no single “required” score that works for every lender or every financial product.

If Your Goal Is Getting Approved for a Credit Card

Many credit card issuers approve applicants with scores in the 670+ range.

However, premium travel cards and high-reward credit cards often require stronger credit profiles.

Aim for:

- Minimum target: 670

- Ideal target: 740+

A stronger score may increase your approval odds and help you qualify for better rewards and lower APRs.

If Your Goal Is Buying a Car

Auto lenders often work with a wide range of borrowers.

Although financing may be available with lower scores, borrowers with 740 or higher typically qualify for more competitive interest rates, reducing the total cost of the loan.

A good target is:

- Acceptable: 670+

- Excellent financing opportunities: 740+

If Your Goal Is Buying a Home

Mortgage lenders generally place significant emphasis on credit scores because home loans involve large borrowing amounts and long repayment periods.

While some loan programs accept much lower scores, borrowers with scores around 760 or above often qualify for the most competitive mortgage rates. Even relatively small differences in interest rates can save tens of thousands of dollars over the life of a mortgage.

Recommended targets:

- Minimum competitive range: 680–700

- Excellent rates: 760+

If Your Goal Is Paying Less Interest

Many people focus only on loan approval.

But approval isn’t the real objective.

The real goal is minimizing borrowing costs.

As your credit score improves, lenders often offer:

- Lower APRs

- Higher borrowing limits

- Better repayment terms

- Greater financial flexibility

Improving your score from “Good” to “Very Good” can sometimes save more money than simply negotiating with a lender.

Is an 800+ Credit Score Necessary?

Not for most people.

An exceptional credit score is certainly impressive, but many borrowers receive excellent loan offers long before reaching 800.

For most financial goals:

- 670 gets you into good standing.

- 740 opens the door to many of the best lending opportunities.

- 760–800 often delivers the strongest available rates.

Beyond that point, the additional financial benefit may be relatively small compared with the effort required to achieve a near-perfect score.

Factors That Matter More Than the Number Alone

Your credit score is important, but lenders also evaluate:

- Your income

- Your debt-to-income ratio (DTI)

- Your employment stability

- Your credit history length

- Your recent credit applications

A strong overall financial profile often matters just as much as your score.

How to Reach Your Target Credit Score

Building better credit takes consistency.

The most effective strategies include:

- Pay every bill on time.

- Keep credit utilization low.

- Avoid unnecessary credit applications.

- Maintain older credit accounts when appropriate.

- Review your credit reports regularly for errors.

If you’re just beginning your credit improvement journey, our guide on How Long It Takes to Improve Your Credit Score explains what you can realistically expect.

How Debt Affects Your Credit Score

High credit card balances can significantly reduce your score because they increase your credit utilization ratio.

If you’re carrying substantial debt, paying it down is often one of the fastest ways to improve your credit profile.

Depending on your situation, these guides may help:

Focus on Financial Progress, Not Perfection

Many people become obsessed with reaching an 850 credit score.

In reality, financial success isn’t determined by having a perfect number.

It’s determined by consistently making smart financial decisions.

A strong budget, responsible borrowing, disciplined spending, and timely payments will naturally move your score higher over time.

As your financial habits improve, your credit score usually follows.

Final Thoughts

The ideal credit score depends on your goals.

If you’re looking for general borrowing flexibility, aim for at least 670.

If you want access to many of the best loan and credit card offers, target 740 or higher.

If you’re preparing for a mortgage or want the lowest available borrowing costs, reaching the 760–800 range can provide meaningful long-term savings.

Remember, your credit score isn’t the destination.

It’s simply one measurement of your overall financial health—and good financial habits will always be more valuable than chasing a perfect number.