The 30-60-90 Day Debt Elimination Plan: A Step-by-Step Roadmap to Financial Freedom

Getting out of debt can feel overwhelming.

Many people know they need to pay off debt, but they don’t know where to start. Others begin with enthusiasm but lose momentum after a few weeks.

The solution is not simply having a goal.

The solution is having a clear plan.

That’s where a 30-60-90 day debt elimination strategy can make a significant difference.

Rather than viewing debt freedom as a distant objective, this approach breaks the journey into manageable milestones that create momentum and measurable progress.

In this guide, you’ll learn exactly what to do during your first 30, 60, and 90 days to build a sustainable debt payoff system and move closer to long-term financial freedom.

Before beginning, make sure you understand the fundamentals of Money Management and Budgeting, because every successful debt payoff strategy starts with controlling cash flow.

Why a 30-60-90 Day Plan Works

Large financial goals often fail because they feel too far away.

When people focus only on becoming debt-free, they may become discouraged by the size of the challenge.

A structured 30-60-90 day plan creates:

- Short-term wins

- Clear priorities

- Measurable progress

- Improved motivation

- Better financial habits

Instead of thinking about years of debt payments, you focus on the actions you can take today.

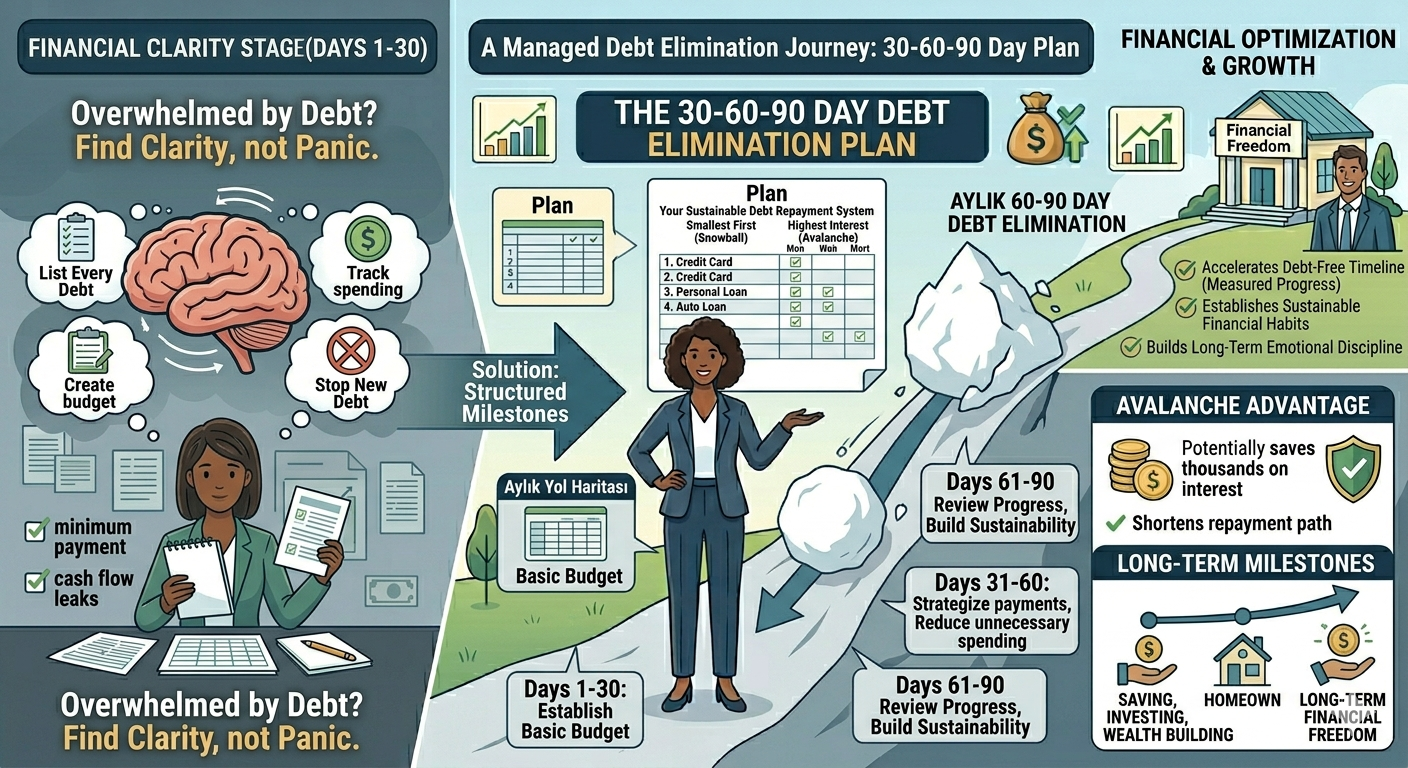

Days 1–30: Build Financial Awareness

The first month is about understanding your financial situation.

You cannot solve a problem you haven’t fully defined.

Step 1: List Every Debt

Create a complete inventory of your debt.

Include:

- Current balance

- Interest rate

- Minimum payment

- Due date

Many people underestimate how much they owe until they see everything in one place.

Step 2: Track Every Dollar

For the next 30 days, monitor all spending.

Every purchase matters.

This process often reveals spending leaks that can be redirected toward debt repayment.

Step 3: Create a Basic Budget

Your budget should prioritize essential expenses while identifying opportunities to increase debt payments.

If you need help building one, our guide on Money Management and Budgeting provides a step-by-step framework.

Step 4: Stop Accumulating New Debt

This may be the most important rule of the entire plan.

Paying off debt while creating new debt is like trying to fill a bucket with a hole in the bottom.

Days 31–60: Attack Debt Strategically

Once you understand your financial situation, it’s time to take action.

Choose Your Debt Payoff Method

At this stage, select a repayment strategy.

The two most popular approaches are:

- Debt Snowball Method

- Debt Avalanche Method

The Debt Snowball Method focuses on paying off the smallest balances first to build momentum.

The Debt Avalanche Method targets the highest-interest debt first to minimize borrowing costs.

Find Extra Cash Flow

Review your spending habits and identify areas where expenses can be reduced.

Even small adjustments can accelerate debt repayment.

Understanding your Spending Habits is often one of the fastest ways to uncover additional money for debt reduction.

Automate Payments

Automatic payments reduce the risk of missed due dates and help maintain consistency.

Days 61–90: Build Long-Term Momentum

The final phase focuses on sustainability.

By now, you should have a clearer understanding of your finances and a functioning debt repayment system.

Review Progress

Compare your current balances with where you started.

Even small reductions represent meaningful progress.

Celebrate wins without undermining your plan.

Strengthen Financial Habits

Debt elimination is not just about numbers.

It is about behavior.

This is why understanding financial psychology is so important.

As discussed in our article on Investment Psychology, long-term success often depends on emotional discipline rather than financial knowledge alone.

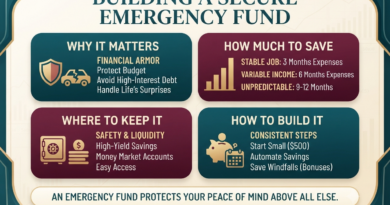

Start Building an Emergency Fund

Unexpected expenses are one of the most common reasons people fall back into debt.

Even a modest emergency fund can create financial stability.

Our guide on Saving Money and Building Financial Security explains how to begin.

Common Mistakes to Avoid

Trying to Do Everything at Once

Debt freedom is a marathon, not a sprint.

Focus on consistency instead of perfection.

Ignoring Small Wins

Progress creates motivation.

Recognizing milestones helps maintain momentum.

Not Having Clear Financial Goals

People are more likely to stay committed when debt repayment is connected to a larger purpose.

Whether your goal is investing, homeownership, retirement, or financial independence, clear objectives matter.

Our guide on Financial Goals can help define your long-term vision.

What Happens After 90 Days?

By the end of the first 90 days, you may not be completely debt-free.

But you will have something equally valuable:

- A structured budget

- A debt repayment strategy

- Improved spending awareness

- Better financial habits

- Clear financial direction

These foundations often determine whether long-term success becomes possible.

Debt Freedom and Financial Freedom

Every debt payment moves you one step closer to financial independence.

As balances shrink, more of your income becomes available for saving, investing, and wealth building.

This is why debt elimination is often one of the most important stages on the path toward Financial Freedom.

The goal is not simply to owe less money.

The goal is to create more choices, flexibility, and control over your future.

Final Thoughts

Becoming debt-free doesn’t happen overnight.

But it does happen through consistent action.

A 30-60-90 day debt payoff plan transforms a massive financial challenge into manageable steps.

Focus on awareness during the first month, action during the second, and long-term habits during the third.

Repeat the process, stay disciplined, and continue moving forward.

Because financial freedom is rarely achieved through one big decision.

It is built through hundreds of small, intentional choices over time.