The Smartest Credit Card Strategy: Using Credit Cards as a Wealth-Building Tool Instead of a Debt Trap

Credit cards have a reputation problem.

For some people, they represent convenience, rewards, and financial flexibility.

For others, they symbolize debt, stress, and financial mistakes.

The reality is that a credit card is neither good nor bad.

It is simply a financial tool.

And like any tool, its value depends on how it is used.

The most financially successful individuals often use credit cards very differently from the average consumer.

They do not view credit cards as borrowing tools.

They view them as cash-flow management tools, credit-building tools, and reward-generating assets.

In this guide, you’ll learn how to use credit cards strategically so they support wealth creation instead of becoming a source of long-term debt.

Before discussing advanced credit card strategies, it’s important to understand the fundamentals of Money Management and Budgeting, because even the best credit strategy cannot compensate for poor financial habits.

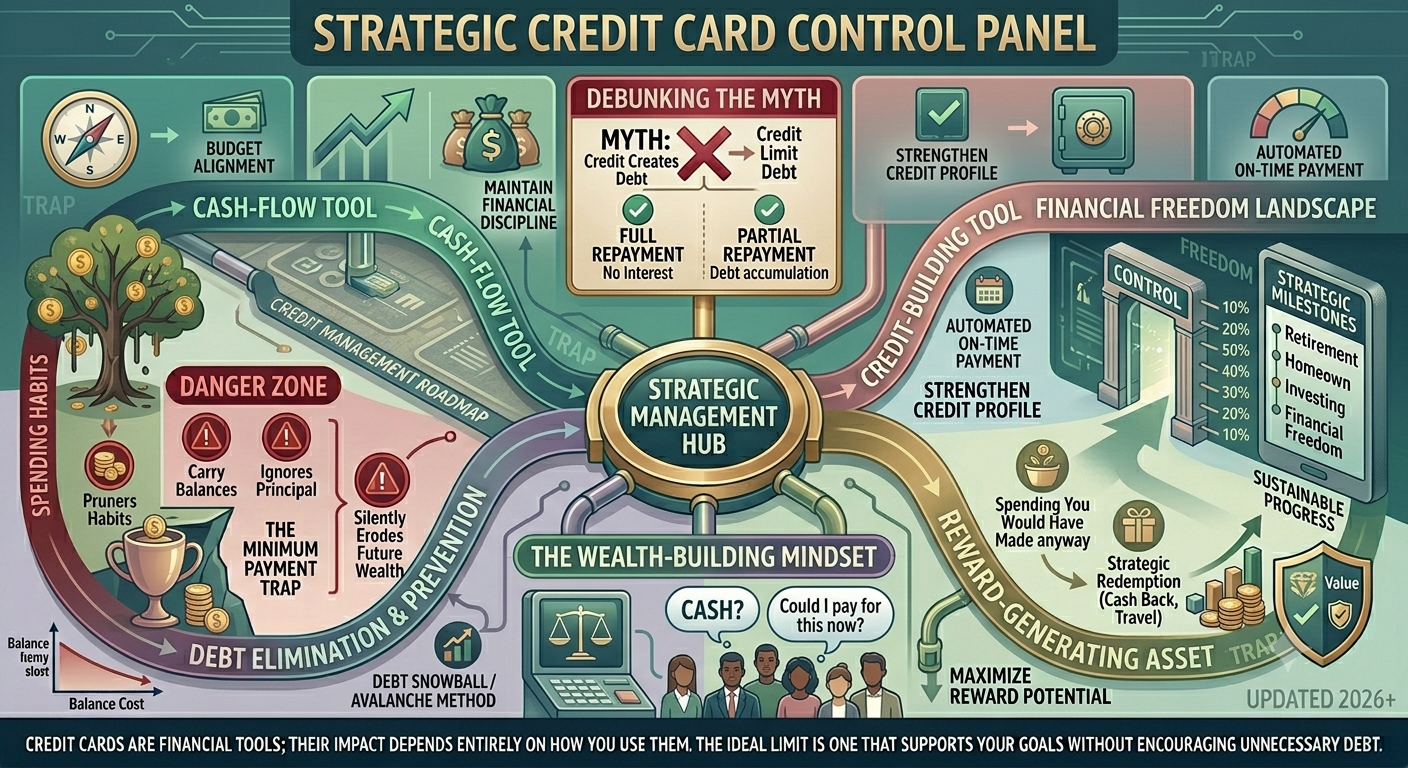

The Biggest Credit Card Myth

Many people believe that using a credit card automatically creates debt.

It does not.

Debt occurs when purchases are not fully repaid.

A credit card simply provides temporary access to funds.

If balances are paid in full every month, interest charges can often be avoided entirely.

This distinction is crucial.

The goal should not be avoiding credit cards.

The goal should be avoiding unnecessary interest payments.

The Wealth-Building Mindset

Financially successful credit card users think differently.

Before making a purchase, they ask:

“Could I pay for this with cash right now?”

If the answer is no, they often avoid the purchase altogether.

In other words, they treat credit cards as a payment method—not a financing method.

This simple shift in mindset dramatically reduces the risk of debt accumulation.

Rule #1: Always Pay the Full Statement Balance

This is arguably the most important rule of credit card management.

Paying the full statement balance each month helps:

- Avoid interest charges

- Maintain financial discipline

- Protect cash flow

- Prevent long-term debt accumulation

Once interest begins accumulating, rewards and benefits often become irrelevant.

The cost of borrowing can quickly exceed any rewards earned.

Rule #2: Never Rely on Minimum Payments

Minimum payments create the illusion of progress while often extending debt repayment for years.

As explained in our guide on the Minimum Payment Trap, this habit can dramatically increase total interest costs.

The minimum payment should be viewed as an emergency fallback—not a long-term strategy.

Rule #3: Keep Credit Utilization Low

Credit utilization is one of the most important factors affecting your credit profile.

Utilization measures how much of your available credit you are currently using.

For example:

- $2,000 balance on a $10,000 limit = 20% utilization

- $5,000 balance on a $10,000 limit = 50% utilization

Lower utilization ratios generally support stronger credit health.

Many experts recommend staying below 30%, while lower levels may provide additional benefits.

For a deeper understanding, read our guide on Choosing the Right Credit Card Limit.

Rule #4: Use Rewards Strategically

Rewards programs can provide meaningful value when used responsibly.

Common benefits include:

- Cash back

- Travel rewards

- Airline miles

- Hotel points

- Purchase protection

However, rewards should never justify unnecessary spending.

Spending $100 to earn $2 in rewards is not a winning strategy.

The best rewards come from purchases you would have made anyway.

Rule #5: Automate Payments

Missed payments can result in:

- Late fees

- Interest charges

- Credit score damage

Setting up automatic payments can help eliminate these risks while simplifying financial management.

Rule #6: Track Spending Consistently

One of the hidden dangers of credit cards is that spending can feel less tangible than using cash.

This psychological effect often leads to overspending.

Regular spending reviews help maintain awareness and control.

If you’re looking to improve financial discipline, our guide on Spending Habits explores how daily financial behaviors influence long-term outcomes.

Rule #7: Align Credit Card Use with Your Budget

A credit card should support your budget—not replace it.

Every purchase should already have a place within your financial plan.

If you don’t currently use a structured budget, start with our guide on Creating a Realistic Monthly Budget.

The strongest credit card strategy is built on a strong budgeting system.

How Credit Cards Can Improve Your Credit Score

Responsible credit card use can help build a stronger credit profile over time.

Positive factors include:

- On-time payments

- Low utilization rates

- Long account history

- Responsible credit management

These factors often contribute to better borrowing opportunities in the future.

To learn more, see our article on Credit Scores and Financial Reputation.

When Credit Cards Become Dangerous

Even powerful financial tools can become harmful when misused.

Warning signs include:

- Carrying balances month after month

- Making only minimum payments

- Using credit cards for routine living expenses

- Frequently reaching credit limits

- Borrowing to maintain a lifestyle

If these patterns continue, debt can accumulate quickly.

Credit Cards and Financial Freedom

Many people assume financial freedom means avoiding credit entirely.

In reality, financial freedom is about control.

A disciplined credit card user can benefit from convenience, security, rewards, and credit-building opportunities without paying significant interest.

This approach supports the broader goal of Financial Freedom.

The objective is not to eliminate financial tools.

The objective is to use them wisely.

Final Thoughts

The best credit card strategy is surprisingly simple.

Spend only what you can afford.

Pay balances in full.

Keep utilization low.

Track your spending.

Use rewards intelligently.

When managed this way, a credit card transforms from a potential debt trap into a valuable financial tool.

Because wealth is not built by avoiding every financial product.

It is built by understanding how to use financial products better than most people do.