What Is the 50/30/20 Budget Rule? And Does It Really Work?

Budgeting is one of the most important foundations of personal finance.

Yet for many people, it feels complicated, restrictive, or difficult to maintain over time.

That is why simple frameworks like the 50/30/20 budget rule have become so popular around the world.

It promises a straightforward way to manage money without complex spreadsheets or advanced financial knowledge.

But the real question is:

Does it actually work in real life?

In this guide, we will break down how the 50/30/20 rule works, its strengths and weaknesses, and how to adapt it to your financial situation.

Before applying any budgeting method, it is important to understand the basics of Money Management and Budgeting, because budgeting is the foundation of every financial decision.

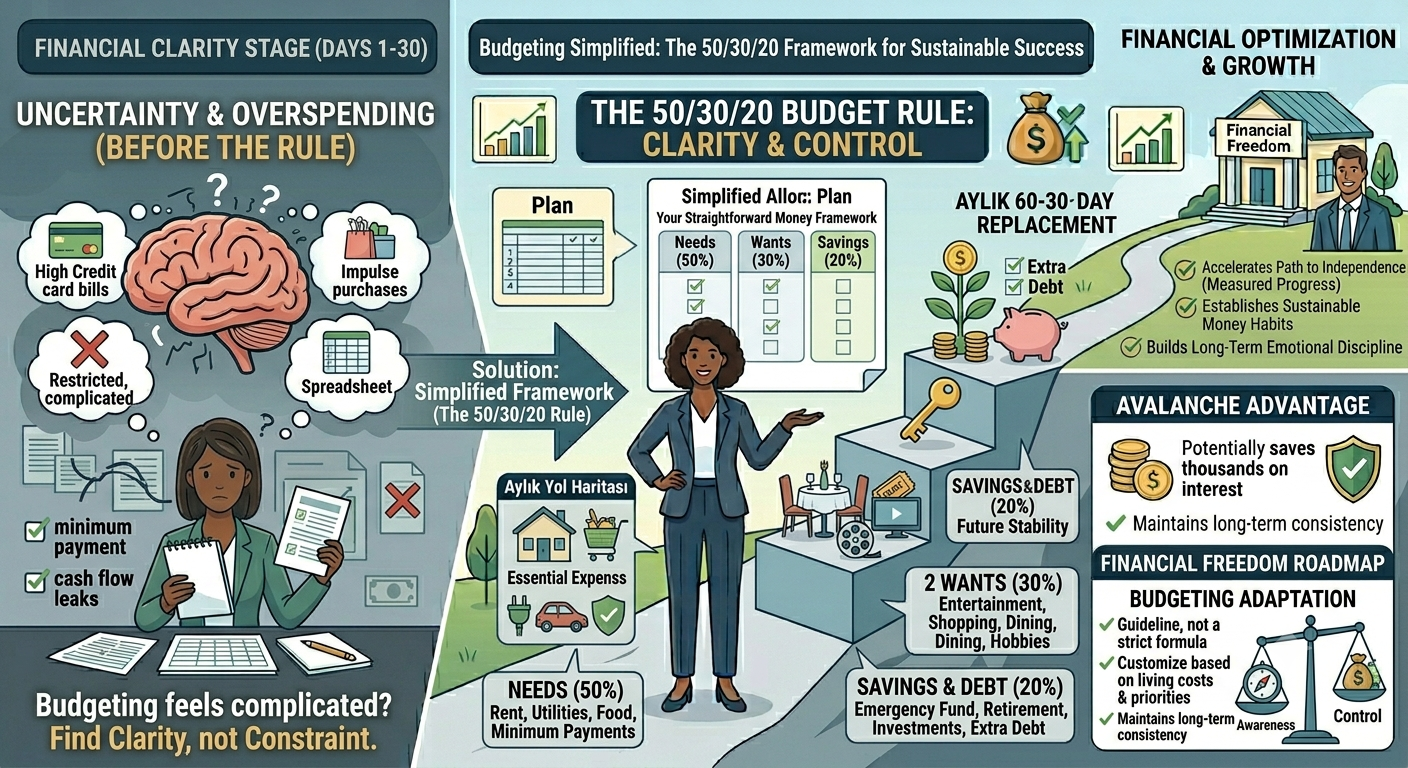

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting framework that divides your after-tax income into three categories:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

This structure was popularized by U.S. Senator Elizabeth Warren and is widely used as a starting point for personal budgeting.

The idea is not precision—it is clarity.

Instead of tracking every expense in detail, you organize your money into three broad buckets.

If you have not yet created a spending plan, start with our guide on How to Create a Monthly Budget.

50% — Needs

This category includes essential expenses you cannot realistically avoid.

Typical examples include:

- Rent or mortgage

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

The goal is to keep these essentials at or below half of your income.

However, in many modern economies, especially in high-cost cities, this threshold can be difficult to maintain.

30% — Wants

This category covers lifestyle spending and non-essential purchases.

Examples include:

- Dining out

- Entertainment

- Streaming services

- Travel

- Hobbies

- Shopping beyond essentials

This is the most flexible category—and also where overspending often happens without notice.

If you frequently exceed this category, our guide on Spending Habits explains how everyday behaviors shape long-term financial success.

20% — Savings and Debt Repayment

This portion is dedicated to building your financial future.

It includes:

- Emergency fund contributions

- Retirement savings

- Investment accounts

- Extra debt payments beyond minimums

This category plays a critical role in long-term financial stability.

If you’re working on debt reduction strategies, you can explore our detailed guide on Debt Elimination Planning.

You may also benefit from our guides on the Debt Snowball Method and the Debt Avalanche Method.

Why the 50/30/20 Rule Became So Popular

The main reason this rule became widely adopted is simplicity.

Most budgeting systems fail because they are too complex to maintain consistently.

This rule avoids that problem by offering a clear structure anyone can apply immediately.

It helps people quickly understand whether their spending is balanced or not.

For example:

- If needs exceed 50%, your fixed costs may be too high.

- If wants exceed 30%, discretionary spending may be out of control.

- If savings are below 20%, long-term goals may be at risk.

Does the 50/30/20 Rule Really Work?

The answer is: it depends.

For some people, it works extremely well as a starting framework.

For others, especially those with low income, high living costs, or significant debt, it may not be realistic without adjustments.

Modern financial research and real-world data show that many households spend more than 50% of income on essential expenses alone.

This means the rule should be treated as a guideline—not a strict formula.

When the Rule Works Best

The 50/30/20 rule is most effective when:

- Your income comfortably covers basic needs.

- You have stable employment.

- You do not carry excessive high-interest debt.

- You are building long-term savings discipline.

In these cases, it provides a strong structure for financial balance.

When the Rule Falls Short

The rule becomes harder to apply when:

- Housing costs are very high.

- Debt obligations already exceed 20%.

- Your income is irregular or unpredictable.

- Unexpected expenses are frequent.

If your income changes from month to month, our guide on How to Budget with an Irregular Income offers practical strategies for building a flexible financial plan.

How to Adapt the 50/30/20 Rule

Instead of treating the rule as fixed, many financial experts recommend adjusting it based on your situation.

For example:

- 60/30/10 for high-cost living areas.

- 50/20/30 when debt repayment is a priority.

- 70/20/10 during aggressive savings phases.

The key is not the exact numbers—it is maintaining awareness and control over your money.

How It Connects to Financial Freedom

Budgeting is not just about tracking spending.

It is about creating a system that supports long-term financial independence.

By consistently managing your income allocation, you build the foundation for financial freedom.

Don’t forget to build your emergency savings along the way. Our guide on Saving Money and Financial Security explains why cash reserves are essential for long-term stability.

You can also learn more about long-term wealth building in our guide on Financial Freedom.

Final Thoughts

The 50/30/20 rule is not a perfect system—but it is a powerful starting point.

Its strength lies in simplicity, not precision.

It helps you see the bigger picture of your financial life without getting lost in complexity.

But like any financial tool, it must be adapted to your reality.

The most important step is not following the rule perfectly.

It is developing awareness, discipline, and consistency in how you manage money.

Because in the end, financial success is not about rigid rules.

It is about sustainable habits.