Family Budgeting: The Art of Planning Your Financial Future Together

Managing money as an individual is already challenging.

Managing money as a family is even more complex.

Different needs, shared responsibilities, and changing priorities make financial planning more difficult—but also more important.

A well-structured family budget is not just about tracking expenses. It is about creating financial harmony, reducing stress, and ensuring that every member of the household is aligned toward the same financial future.

In this guide, we’ll explore what a family budget is, why it matters, and how to build one that actually works in real life.

If you are new to financial planning, it is helpful to first understand the basics of Money Management and Budgeting and how financial behavior connects to long-term outcomes.

What Is a Family Budget?

A family budget is a financial plan that outlines how a household earns, spends, saves, and invests money over a specific period, usually a month.

It helps families understand their cash flow and make intentional financial decisions together.

A family budget typically includes:

- Total household income

- Fixed expenses (rent, utilities, insurance, loans)

- Variable expenses (food, transportation, entertainment)

- Savings and investments

- Emergency fund contributions

Unlike personal budgeting, a family budget requires coordination between multiple people, which makes communication and structure essential.

Why Family Budgeting Matters

Without a family budget, financial decisions are often made reactively instead of strategically.

This leads to:

- Overspending in some categories

- Lack of savings consistency

- Financial stress between family members

- Difficulty achieving long-term goals

With a family budget, every dollar has a purpose. This creates clarity, stability, and shared accountability.

Financial success in a household is not only about income—it is about alignment. That is why setting clear priorities through Financial Goals is essential for every family.

Key Components of a Strong Family Budget

1. Income Tracking

The first step is understanding total household income from all sources, including salaries, side income, and investments.

2. Fixed Expenses

These are recurring and predictable costs such as rent, mortgage payments, insurance, and subscriptions.

3. Variable Expenses

These include groceries, transportation, dining out, and entertainment—categories that change month to month. Monitoring your spending habits makes these expenses much easier to control.

4. Savings and Investments

A strong family budget always includes savings goals and long-term investment contributions. Developing consistent saving behavior becomes much easier when you follow the principles in our Ultimate Saving Guide.

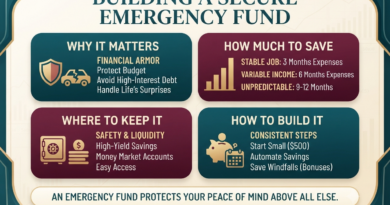

5. Emergency Fund

Most financial experts recommend setting aside three to six months of essential expenses to protect against unexpected events and strengthen your path toward financial freedom.

Popular Family Budgeting Methods

The 50/30/20 Rule

One of the most widely used budgeting frameworks in the United States is the 50/30/20 Rule:

- 50% for needs

- 30% for wants

- 20% for savings and investments

This method provides a simple structure for balancing daily living with long-term financial growth.

Zero-Based Budgeting

In this method, every dollar of income is assigned a purpose so that income minus expenses equals zero.

This ensures maximum awareness and control over household spending.

Envelope System

This approach allocates cash or virtual “envelopes” for different spending categories, helping families control overspending in specific areas and avoid impulse spending.

How to Build an Effective Family Budget

Step 1: Calculate Total Income

Start by identifying all sources of monthly income after taxes.

Step 2: List All Expenses

Track fixed and variable expenses for at least one month to understand spending patterns.

If you need a practical framework, follow our guide on creating a realistic monthly budget.

Step 3: Set Financial Priorities

Decide together what matters most—debt repayment, saving, investing, or short-term goals.

Step 4: Create a Spending Plan

Allocate income into categories based on priorities and financial goals.

This step becomes significantly easier when aligned with clear objectives. If you need help defining them, read our guide on Financial Goals.

Step 5: Review and Adjust Monthly

A family budget is not static. It should evolve as income, expenses, and life circumstances change.

Common Challenges in Family Budgeting

Different Spending Habits

Each family member may have different financial behaviors, which can lead to conflict without clear rules.

Irregular Expenses

Unexpected costs such as medical bills, car repairs, or school expenses can disrupt even the best budget.

Lack of Communication

Without regular financial discussions, budgets often fail due to misalignment between partners or family members.

How Family Budgeting Builds Long-Term Wealth

A family budget is not just about controlling expenses—it is about building wealth systematically.

When households consistently track spending, save regularly, and invest wisely, they create financial momentum over time.

Even small improvements in saving habits can lead to significant long-term results when combined with disciplined investing and a healthy investment psychology.

Strong budgeting habits also reinforce better financial behavior across generations, helping children develop healthy money habits early in life.

Final Thoughts

A family budget is more than a financial tool—it is a shared roadmap for financial stability and growth.

It helps families reduce stress, improve communication, and achieve long-term financial goals together.

When combined with strong money management practices and clear financial objectives, it becomes one of the most powerful tools for building lasting wealth.

Financial success at the household level is not about perfection.

It is about consistency, alignment, and intentional decision-making.