Emergency Fund: The Financial Safety Net Everyone Needs

Life rarely goes exactly as planned.

Your car breaks down.

You lose your job.

A medical bill arrives unexpectedly.

Your home needs an urgent repair.

Financial emergencies aren’t a matter of if—they’re a matter of when.

The difference between a temporary setback and a long-term financial crisis often comes down to one thing:

An emergency fund.

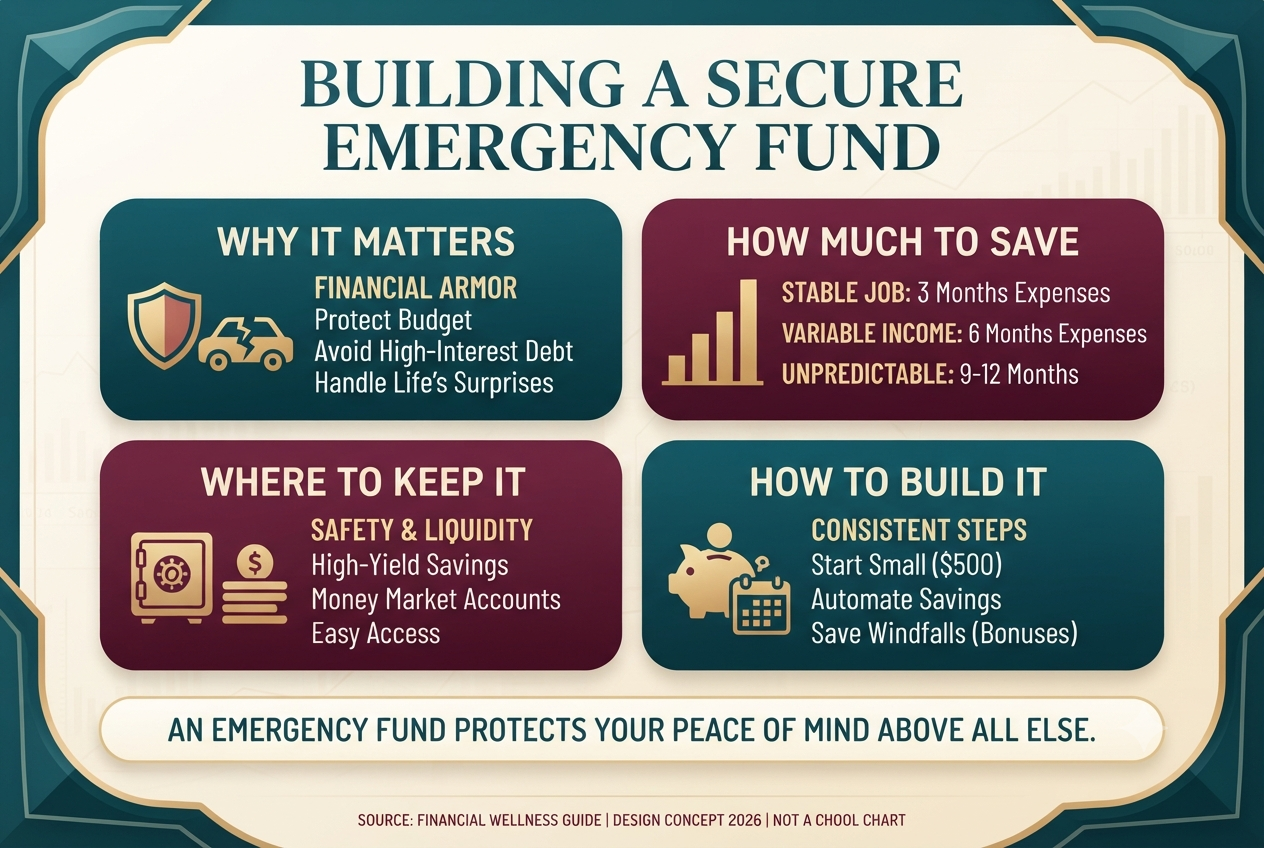

An emergency fund acts like financial armor. It protects you from turning unexpected expenses into long-term debt and gives you the confidence to navigate life’s surprises without derailing your financial future.

In this guide, you’ll learn what an emergency fund is, how much you should save, where to keep it, and how to build one—even if you’re starting from zero.

Before building an emergency fund, make sure your overall financial plan is on solid ground with our guide to Money Management and Budgeting. You’ll also benefit from creating a realistic monthly budget that consistently sets aside money for unexpected events.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected expenses or temporary income loss.

Unlike your regular savings, this money has one purpose:

To help you handle genuine financial emergencies without relying on credit cards or loans.

Typical emergencies include:

- Job loss.

- Unexpected medical expenses.

- Major car repairs.

- Essential home repairs.

- Emergency travel for family situations.

- Unexpected income interruptions.

An emergency fund should not be used for vacations, holiday shopping, or planned purchases. It is intended only for genuine financial emergencies.

Why an Emergency Fund Is So Important

Without emergency savings, even a relatively small financial shock can become expensive.

Many people respond to emergencies by:

- Using high-interest credit cards.

- Taking out personal loans.

- Borrowing from retirement savings.

- Selling investments at the wrong time.

An emergency fund allows you to solve today’s problem without creating tomorrow’s financial burden. It also helps you avoid being forced to sell long-term investments during market downturns. If you’re already dealing with debt, our 30-60-90 Day Debt Elimination Plan can help you regain control while building financial resilience.

How Much Should You Save?

There’s no single amount that’s right for everyone.

Your ideal emergency fund depends on your income, expenses, job stability, and family responsibilities.

As a general guideline:

- 3 months of essential living expenses if you have stable employment.

- 6 months of expenses if you’re self-employed, have variable income, or support a family.

- 9–12 months if your income is highly unpredictable or finding new employment may take longer.

Financial institutions generally recommend saving three to six months of essential expenses, while households with less predictable income may benefit from an even larger cushion. If your earnings fluctuate throughout the year, see our guide on Budgeting with an Irregular Income.

Where Should You Keep Your Emergency Fund?

Your emergency savings should prioritize three qualities:

- Safety.

- Liquidity.

- Easy access.

For most people, the best options include:

- High-yield savings accounts.

- Money market accounts.

- Federally insured bank or credit union savings accounts.

Avoid investing your emergency fund in stocks or other volatile assets. Market declines can reduce your savings precisely when you need the money most.

How to Build an Emergency Fund

1. Start Small

You don’t need thousands of dollars on day one.

Your first goal might simply be:

- $500

- $1,000

- One month’s expenses

Every dollar saved reduces future financial stress.

2. Automate Your Savings

Set up an automatic transfer every payday.

Even $25 or $50 per week adds up over time and removes the temptation to spend the money elsewhere.

3. Save Windfalls

Consider directing unexpected money toward your emergency fund, such as:

- Tax refunds.

- Work bonuses.

- Cash gifts.

- Freelance income.

These lump sums can accelerate your progress without affecting your normal monthly budget.

You’ll find additional practical ideas in our guide on The Power of Small Savings, which explains how consistent habits build long-term financial security.

When Should You Use Your Emergency Fund?

Ask yourself these questions before using your savings:

- Is this expense unexpected?

- Is it necessary?

- Can it wait?

If the answer is yes to the first two and no to the third, your emergency fund is probably the right solution.

Remember, using your emergency fund for a true emergency isn’t a failure—it’s exactly why you built it. The key is to replenish it afterward.

Emergency Fund vs. Investing

Many new investors ask whether they should invest first or build an emergency fund first.

In most cases, building at least a basic emergency fund should come first.

Without cash reserves, an unexpected expense may force you to sell investments during a market downturn or rely on high-interest debt.

Once you’ve established a solid emergency cushion, you can confidently focus on long-term investing.

Our guide to The Power of Small Savings explains how consistent saving creates the foundation for long-term wealth.

Common Emergency Fund Mistakes

- Investing emergency savings in risky assets.

- Keeping the money in your everyday checking account.

- Using the fund for vacations or impulse purchases.

- Never rebuilding the fund after using it.

- Waiting for the “perfect time” to start saving.

The biggest mistake is believing you need a large amount before getting started.

Starting small today is far better than waiting indefinitely.

How an Emergency Fund Supports Financial Freedom

An emergency fund provides more than financial protection.

It gives you confidence.

You can make career decisions without immediate financial panic.

You can handle life’s surprises without accumulating expensive debt.

You can stay focused on long-term investing instead of constantly reacting to short-term crises.

Our guide to Financial Freedom explores how emergency savings fit into a complete wealth-building strategy.

Final Thoughts

An emergency fund isn’t exciting.

It won’t produce stock market returns or make headlines.

But it may be the single most valuable financial asset you ever build.

It protects your budget.

It protects your investments.

Most importantly, it protects your peace of mind.

Start with whatever amount you can save today.

Stay consistent.

Over time, your emergency fund will become the financial safety net that allows every other part of your financial plan to grow with confidence.