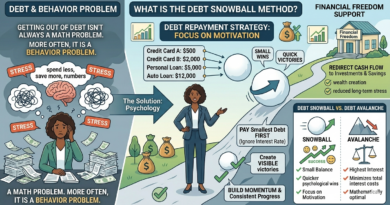

Spending Habits: The True Architect of Your Financial Future

Most people believe that financial success depends on how much money they earn.

But in reality, your financial future is shaped far more by how you spend money than how much you make.

Two people with the same income can end up in completely different financial positions—simply because of their spending habits.

One builds wealth. The other struggles paycheck to paycheck.

The difference is not intelligence or opportunity. The difference is behavior.

In this article, we will explore how spending habits shape your financial life, why they matter more than income, and how you can take control of them to build long-term financial stability.

If you want to build a strong financial foundation, it helps to first understand the basics of Money Management and Budgeting and how your financial decisions connect to long-term outcomes.

What Are Spending Habits?

Spending habits are the patterns and behaviors that determine how you use your money.

They include everything from daily coffee purchases to major financial decisions like buying a car or choosing a mortgage.

Most spending habits are not conscious decisions—they are automatic behaviors formed over time.

This is why many people struggle financially even when they earn a good income. Their habits quietly drive their financial decisions without them realizing it.

Why Spending Habits Matter More Than Income

A higher income does not guarantee financial success.

In fact, many people fall into the trap of “lifestyle inflation,” where spending increases every time income increases.

This creates a cycle where financial stress never truly disappears.

For example:

- A person earning $50,000 may spend $45,000 and save very little.

- Another earning $100,000 may spend $95,000 and still feel financially stressed.

The problem is not income. The problem is behavior.

Without controlled spending habits, increased income only leads to increased consumption—not wealth.

This is one of the key reasons why financial planning must include clear objectives. You can learn more about this in our guide on Financial Goals.

The Psychology Behind Spending Habits

Spending is not just a financial activity—it is a psychological one.

People spend money for emotional reasons such as:

- Stress relief

- Social acceptance

- Instant gratification

- Reward behavior

This is why budgeting alone often fails. Without addressing your financial psychology, the same spending patterns tend to repeat.

Modern consumer culture is also designed to encourage spending. One-click purchases, credit cards, and digital payment systems remove friction and make spending feel effortless.

Common Types of Spending Habits

1. Impulse Spending

Impulse spending happens when purchases are made without planning.

These are often small purchases that feel harmless individually but add up significantly over time. Learning how to stop impulse spending can dramatically improve your financial future.

2. Emotional Spending

Many people spend money to manage emotions like stress, boredom, or sadness.

This type of spending provides short-term relief but long-term financial damage.

3. Lifestyle Inflation

As income increases, expenses automatically rise.

Instead of improving financial stability, higher income simply funds a more expensive lifestyle.

We also explore this concept in depth in our article on building saving habits and financial discipline.

4. Invisible Spending

Subscriptions, small digital payments, and automatic renewals often go unnoticed.

Over time, these “invisible” expenses can become a major part of monthly spending.

How Spending Habits Affect Your Financial Future

Your spending habits directly determine three key outcomes:

- How much you save

- How much you invest

- How quickly you achieve financial freedom

If spending is uncontrolled, savings shrink.

If savings shrink, investment opportunities disappear.

If investment opportunities disappear, long-term wealth becomes difficult to build.

In other words, spending habits shape your entire financial trajectory.

How to Take Control of Your Spending Habits

1. Track Every Expense

You cannot improve what you cannot measure.

Tracking your expenses for even one month can reveal surprising patterns.

Most people discover that a large portion of their money is spent on non-essential items.

2. Create a Budget That Reflects Reality

A budget is not a restriction—it is a plan for your money.

A well-designed budget helps you understand where your money is going and where it should go.

If you haven’t built one yet, our guide on Money Management and Budgeting can help you get started. You can also follow our step-by-step guide to creating a realistic monthly budget.

3. Apply the 24-Hour Rule

Before making non-essential purchases, wait 24 hours.

This simple delay reduces impulse spending and helps you make more rational financial decisions.

4. Automate Good Financial Behavior

Automation is one of the most powerful tools in personal finance.

By automatically transferring money into savings or investment accounts, you reduce the temptation to spend it.

5. Replace Spending Triggers

If you tend to spend when stressed or bored, replace that behavior with healthier alternatives such as exercise, reading, or learning a new skill.

Changing the trigger is more effective than trying to rely on willpower alone.

Building Wealth Starts With Behavior

Wealth is not built by income alone.

It is built by consistent financial behavior over time.

Small improvements in spending habits can lead to massive long-term results.

For example:

- Reducing unnecessary monthly expenses by $200

- Investing that amount consistently over 20 years

- Allowing compound growth to work in your favor

The difference is not just saving money—it is building financial momentum.

Final Thoughts

Your spending habits are the foundation of your financial life.

They determine whether you build wealth or stay stuck in financial stress.

The good news is that spending habits are not fixed—they can be changed.

By becoming aware of your behavior, creating structure, and making intentional decisions, you can take control of your financial future.

If you combine strong spending habits with proper budgeting and clear financial goals, you create a powerful system for long-term wealth building.

Because in the end, financial success is not about earning more—it is about managing better.