The Power of Small Savings: How Tiny Financial Habits Create Long-Term Wealth

Many people believe they need a high income to build wealth.

They assume saving $10 or $20 here and there won’t make much difference.

But that’s one of the biggest myths in personal finance.

Financial success is rarely built through one massive decision.

Instead, it’s usually the result of hundreds—or even thousands—of small financial choices made consistently over many years.

Those daily decisions compound into something much larger than most people imagine.

In this guide, you’ll discover why small savings matter, how compound growth works in your favor, and practical ways to turn everyday financial habits into long-term wealth.

Every successful savings strategy starts with a plan. If you haven’t already, begin with our guide to Money Management and Budgeting. Once you’ve built that foundation, you can also learn how to create a sustainable Monthly Budget that consistently makes room for saving.

Why Small Savings Matter More Than You Think

People often delay saving because they feel they can’t save “enough.”

They tell themselves they’ll start once they earn more money.

Unfortunately, that mindset delays one of the most valuable financial advantages anyone can have: time.

Saving even small amounts consistently allows your money to benefit from compound growth, where your earnings begin generating earnings of their own. Over long periods, this can dramatically increase your savings and investments.

The Magic of Compound Growth

Compound growth is often called one of the most powerful forces in personal finance.

Here’s why.

Imagine saving $100 every month and investing it consistently.

Each contribution has the opportunity to generate returns.

Over time, those returns begin generating additional returns.

This snowball effect allows relatively small contributions to grow into surprisingly large balances over decades.

The earlier you begin, the longer compounding has to work for you.

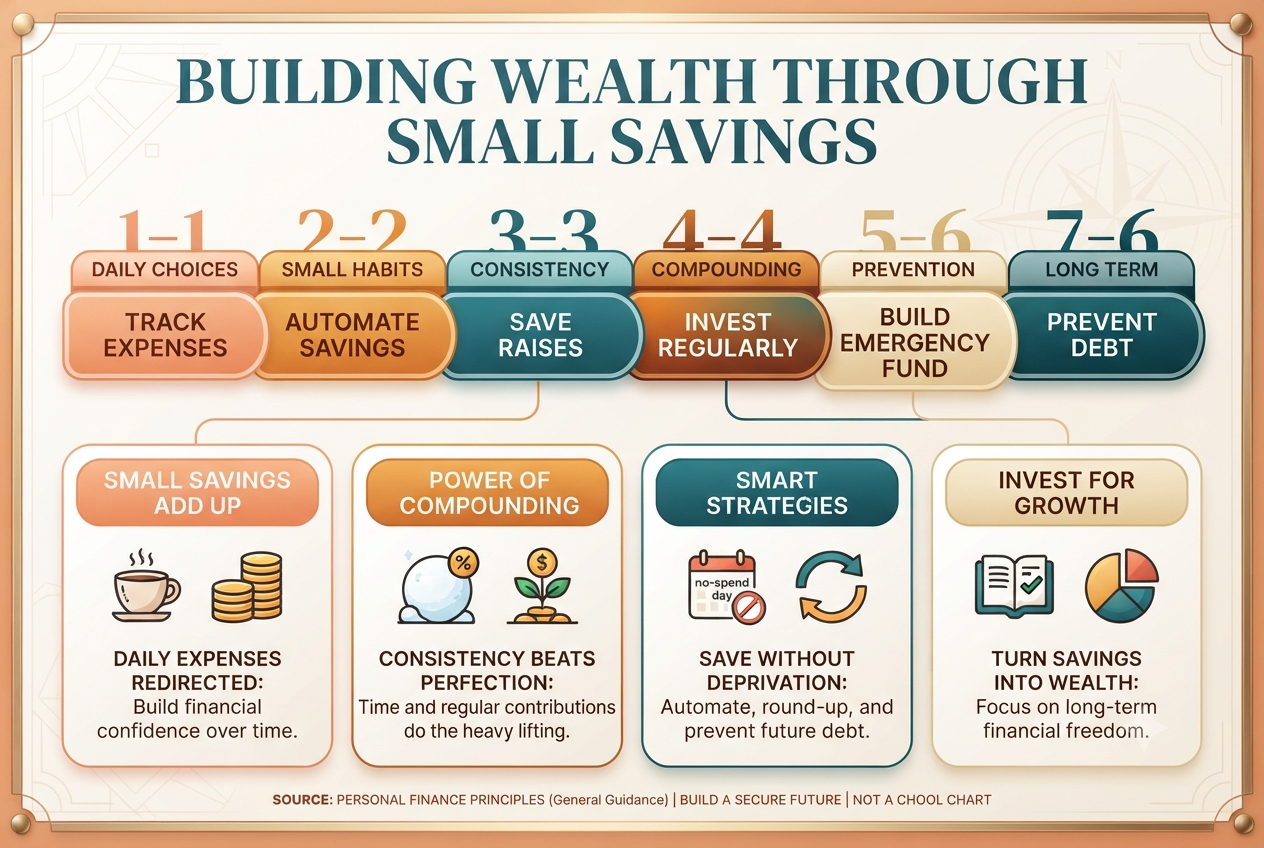

Small Daily Choices Add Up

Think about the small expenses that often go unnoticed:

- A daily specialty coffee.

- Food delivery fees.

- Unused subscriptions.

- Impulse purchases.

- Frequent convenience store visits.

Individually, these expenses may seem insignificant.

Over the course of a year, however, they can easily total hundreds—or even thousands—of dollars.

Redirecting just a portion of those expenses toward savings or investing can significantly improve your long-term financial position. If impulse buying is your biggest challenge, our guide on How to Stop Impulse Spending offers practical techniques to regain control.

Consistency Beats Perfection

Many people believe they need to save large amounts every month.

In reality, consistency is often more important than size.

Saving $50 every month for years is generally more effective than saving $1,000 once and then stopping.

Regular contributions create momentum while allowing compound growth to work continuously.

Practical Ways to Save Without Feeling Deprived

Automate Your Savings

Set up an automatic transfer every payday.

Even a small automatic deposit helps build the habit before you’re tempted to spend the money. Financial experts often refer to this approach as “pay yourself first.”

Round Up Your Purchases

Many financial apps allow you to round purchases up to the nearest dollar and automatically save or invest the difference.

These micro-savings may seem tiny, but they can accumulate surprisingly quickly.

Save Every Raise

Whenever your income increases, direct part of the additional money toward savings instead of increasing your lifestyle spending.

This strategy allows your savings rate to grow without significantly affecting your day-to-day lifestyle.

Create a “No-Spend Day”

Choose one day each week when you spend nothing beyond true necessities.

Over the course of a year, these intentional pauses can free up meaningful amounts of money.

Small Savings Build Financial Confidence

The biggest benefit of saving isn’t always the money itself.

It’s the confidence that comes from knowing you’re making steady progress.

Watching your savings account grow—even slowly—reinforces positive financial habits.

That confidence often leads to better budgeting, smarter investing, and more disciplined spending.

Turn Savings Into Investments

Once you’ve built an emergency fund, additional savings can begin working even harder through long-term investing.

Whether you invest in broad stock market index funds, retirement accounts, or other diversified investments, combining consistent contributions with long-term market growth can significantly increase wealth over time.

Setting clear objectives also helps maintain motivation. Our guide on Financial Goals explains how to connect today’s savings with tomorrow’s ambitions.

Don’t Underestimate Small Wins

Financial progress rarely happens overnight.

It’s built through countless small victories:

- Skipping one unnecessary purchase.

- Saving an extra $20.

- Cooking dinner instead of ordering takeout.

- Investing part of every paycheck.

- Paying yourself first every month.

Each decision may seem minor.

Together, they can completely transform your financial future.

Small Savings Help Prevent Debt

Having even a modest emergency fund reduces the likelihood that unexpected expenses will force you to rely on credit cards or personal loans.

That’s why consistent saving is one of the best forms of financial protection.

If you’re currently working to eliminate debt while building savings, these guides can help:

Keep Your Eyes on the Bigger Picture

Every dollar you save today is a dollar that can work for you tomorrow.

The objective isn’t simply to accumulate money.

It’s to create freedom, flexibility, and peace of mind.

Our guide to Financial Freedom explains how consistent saving becomes the foundation for long-term independence.

Final Thoughts

Building wealth doesn’t require perfect timing or an enormous paycheck.

It requires consistency.

Small savings may not seem exciting today, but given enough time, they become one of the most powerful financial tools available.

Start with whatever you can afford.

Stay consistent.

Let time and compound growth do the heavy lifting.

Because in personal finance, small habits repeated for years almost always outperform big promises that never become reality.